Private Mortgage Lender for Commercial Property

Fast commercial property finance from $250k to $10M. Funded within 24 hours, assessed on the asset, not your trading history.

Specialists in commercial property finance for corporate structures

Secured Lending is a private mortgage lender. We fund commercial property deals that a bank will not do, or cannot do in time. We hold our own credit authority and use our own valuers, so you get an indicative answer the same day and a clean deal can settle inside 24 to 72 hours. We lend to Pty Ltd companies, family trusts, and SMSFs, for business purposes only.

Commercial Property Finance at a Glance

- $250,000 to $10,000,000 and above: Larger transactions assessed on their merits.

- Up to 70% LVR: Higher on strong assets with a clear exit, case by case.

- Terms of 1 to 24 months: Interest-only, from 9.7% p.a., establishment fee 1% to 2%.

- Indicative answer the same day: Settlement from 24 to 72 hours on a clean deal.

- Corporate borrowers only: Business purpose lending, so no NCCP-regulated personal name loans.

- First and second mortgages: Registered over the commercial property title.

Commercial Property We Lend Against

Tenanted, owner-occupied, and vacant assets are all eligible.

- Industrial: Warehouses, logistics facilities, factories, and strata industrial units.

- Retail: Strata shops, showrooms, and large-format retail.

- Office: Whole floors, suites, and strata office in metropolitan and fringe locations.

- Mixed-use: Commercial and residential combined on one title.

- Specialised: Medical centres, childcare, service stations, and hospitality venues.

- Vacant commercial: No lease income required. We assess on security value and exit, not rent roll.

Purchase Types We Fund

- Owner-occupier: A business buying its own premises, including purchases at auction and settlements with a fixed deadline.

- Commercial investment: Investors acquiring or expanding a tenanted commercial portfolio.

Borrower Structures We Fund

- Pty Ltd company: The company holds title, directors provide personal guarantees, full-recourse commercial mortgage.

- Family trust: Discretionary and unit trusts. We review the deed, confirm the trustee's power to borrow, and lend to the trustee entity.

- SMSF: Purchase of business real property via a Limited Recourse Borrowing Arrangement under the SIS Act, coordinated with your adviser and solicitor.

Loan Scenarios We Solve

- Bridging: Fund the settlement now and discharge when your bank facility completes, typically 30 to 90 days.

- Refinance: Move off an expiring, repriced, or unsuitable facility without a bank timeline.

- Equity release: Pull working capital or acquisition funds out of a commercial asset you already hold.

- Second mortgage: Sit behind an existing first, provided the combined LVR stays within 70%.

Situations Banks Struggle With

- Property developers: Site acquisition, settlement shortfalls, and equity release from completed stock to recycle into the next site.

- After a bank decline: Sector policy, entity structure, LVR caps, director credit history, or thin trading history. We assess the asset and the exit instead.

- Approval withdrawn after exchange: We can fund the settlement so the deposit is not at risk.

"On a commercial deal the exit does more work than the asset. We are comfortable funding a vacant warehouse or a childcare centre that a bank has stepped away from, because what we are underwriting is how the loan gets repaid, not whether the building fits a policy category. Where a borrower has thought that through and has the evidence behind it, we can usually come back the same day."

Gino Tabila

Associate Director

What We Need to Assess It

To issue a term sheet we typically need:

- The contract of sale, or title details if you are refinancing.

- Entity documents: company search, trust deed, or SMSF deed and trustee details.

- The current or expected value of the security, and any existing mortgage balance.

- A written exit strategy. This is the single biggest factor in the decision.

A credible exit is specific and achievable inside the term: a sale supported by market evidence, a refinance with a demonstrable pathway, or confirmed proceeds from another transaction. A vague intention to eventually refinance is not an exit strategy.

Residential investment property held in a company, trust, or SMSF is covered on our investment property lending page. For business-purpose facilities secured by property, see secured business loans.

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Are you a broker? Find out why brokers love working with us.

Case Studies

Unlocking Industrial Property Deals: How Flexible $5 Million Funding Secured a Port Adelaide Warehouse

How Secured Lending Facilitated A $2.8 Million Loan For A Commercial Property Acquisition

$1.9M Commercial Property Acquisition for Growing Doggy Daycare Business

$1.3M Second Mortgage Helped Bankstown Industrial Borrower Clear Tax Debt and Refinance

$450,000 Caveat Loan Against Commercial Property Saved Sydney Café From Insolvency

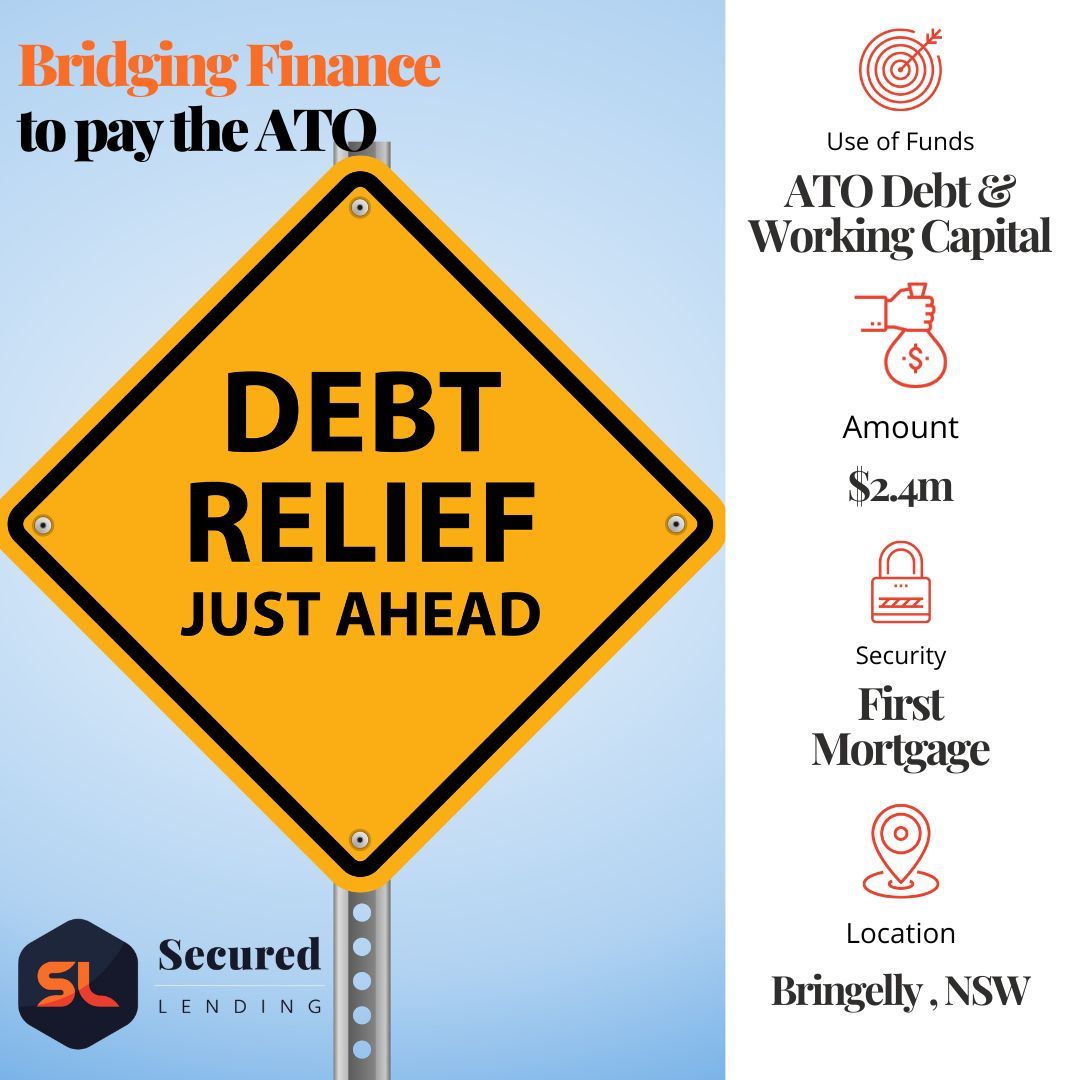

$2.4 Million Bridging Loan for Working Capital: Fast Relief for Small Business Struggling with Cash Flow

$2.5 Million Loan: How Equity Release Finance Can Fuel Your Small Business

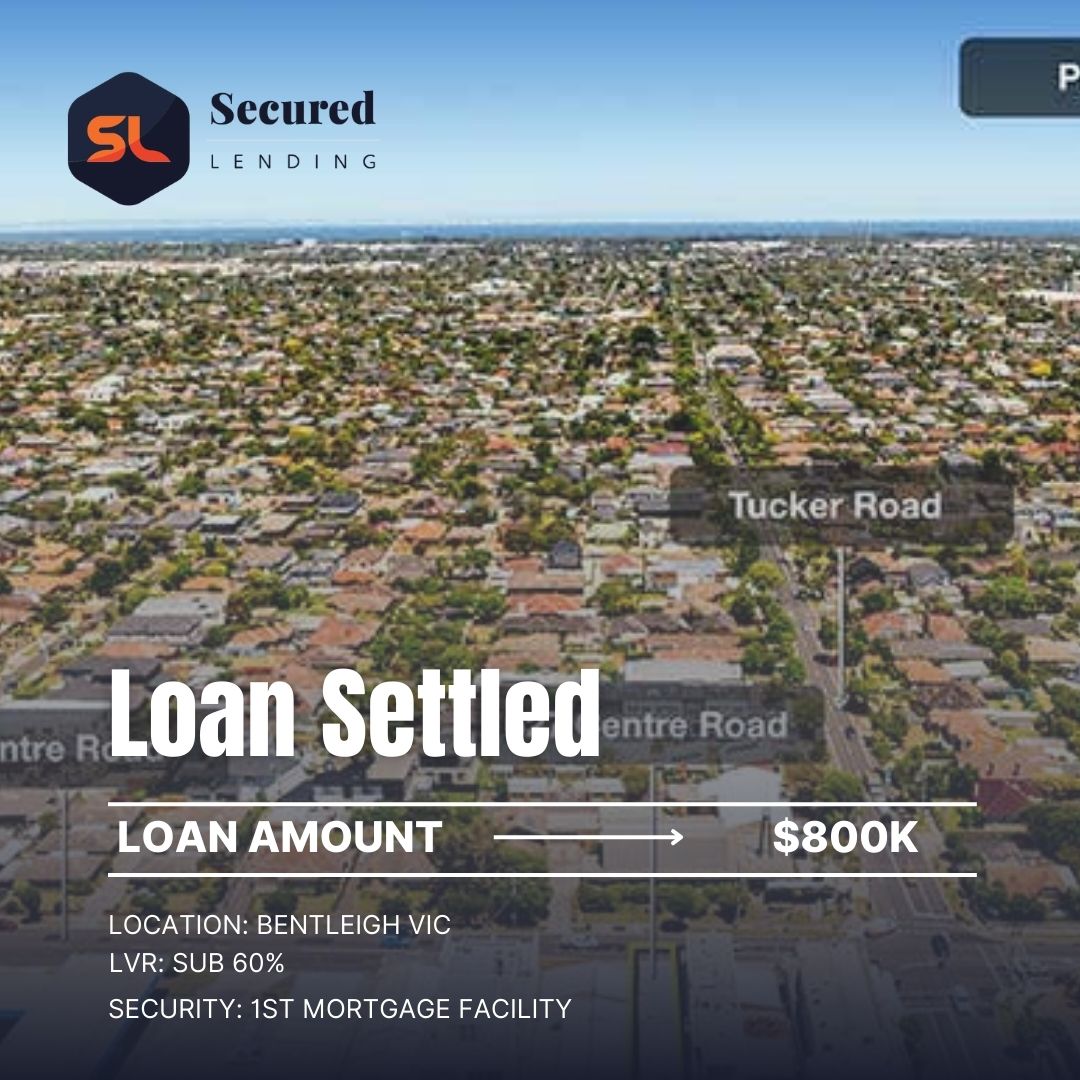

Navigating the Tightrope: When a $800,000 Tax Liability Met a Time-Sensitive Property Play

Frequently Asked Questions

Common questions about using a private mortgage lender for commercial property.

Contact Us