A steady-performing first mortgage income fund

First mortgage lending is the most conservative position in the private lending capital stack, and it is where the SL Premium Income Fund invests exclusively. Every dollar is secured by a registered first mortgage, the senior charge over a property, delivering a target 7% to 9.95% per annum as regular monthly income.

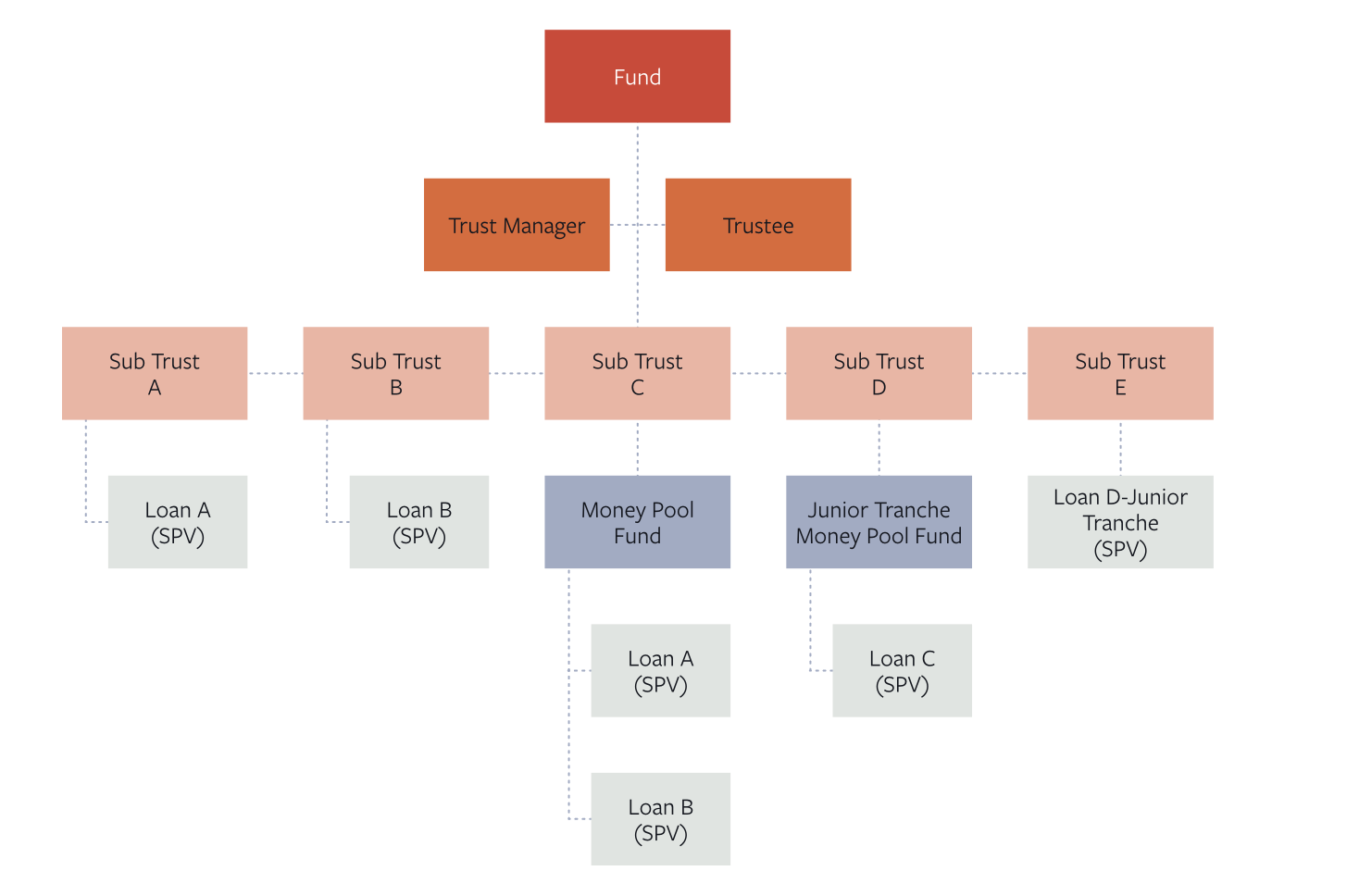

Within the SL Premium Income Fund, every loan is secured by a first-ranking registered mortgage over real property in Australia. The objective is to provide Wholesale and Sophisticated Investors with a monthly income stream through a selection of short-term, first-mortgage loans, prioritising capital preservation alongside an attractive, regular return.

Case Studies

A selection of completed loans funded for our investors, each secured by a registered first mortgage over Australian property.

Minimum investment: $100,000.Available to wholesale and sophisticated investors only. Investments under $500,000 require a qualified accountant’s certificate confirming wholesale or sophisticated investor status.

Completed transactions, shown anonymised. Past performance is not indicative of future returns; investor returns and amounts vary by deal and sub-trust.

Why first-mortgage security matters

The ranking of the mortgage determines who gets repaid first if a loan goes wrong. A first mortgage, combined with a conservative loan-to-value ratio, is what gives a first mortgage income fund its defensive profile.

First-ranking priority

A registered first mortgage is the senior charge over a property. In a recovery, the first mortgagee is repaid before second mortgages, mezzanine debt and unsecured creditors. Where loans are syndicated, the senior first-mortgage tranche prevails over junior tranches for both principal and interest.

A built-in equity buffer

Loans are limited to a maximum 70% loan-to-value ratio. That means the borrower’s equity absorbs the first 30% of any fall in the property’s value before an investor’s capital is exposed.

Supporting security

Beyond the mortgage, loans may be backed by personal guarantees from company directors, third-party corporate guarantees, and general or specific security agreements registered on the PPSR.

Capital-preservation focus

The Trust Manager’s stated aim is to preserve capital and provide regular returns by ensuring loans are secured by registered first mortgages over real property, with appropriate supporting security and guarantees.

Why investors choose mortgage-fund income

For investors seeking regular income without the volatility of listed markets, a first mortgage income fund offers a compelling risk-adjusted profile.

Steady income

Regular interest payments from borrowers translate into a consistent income stream for investors.

Diversification

Mortgage-fund returns are largely uncorrelated with shares and other asset classes, helping diversify a portfolio.

Professional management

Loans are sourced, assessed and managed by an experienced team with deep knowledge of the mortgage market.

Attractive returns

A target 7–9.95% p.a. can exceed the returns of other fixed-income options such as term deposits and bonds.

Lower volatility

Backed by registered first mortgages over real property, returns tend to be more stable through market cycles.

Risk-adjusted returns

A conservative 70% LVR and first-ranking security aim to deliver a strong return for the level of risk taken.

How the income is generated

Income comes from the interest borrowers pay on short-term commercial loans. Because the loans are short, generally under 12 months, and pre-funded by Secured Lending before investors participate, the fund can put capital to work quickly and recycle it as loans are repaid.

Some loans distribute income monthly; others capitalise interest and repay at the end of the term. Across the fund, the target return is 7% to 9.95% per annum, varying by sub-trust to reflect each loan’s risk. Returns are not guaranteed.

The SL Difference

Secured Lending has been dealing in the private lending space since 2016, having grown a substantial portfolio and strong network of brokers, accountants, and financial advisers.

Our flexible and intuitive product allows us to keep up with the ever-changing landscape of commercial finance. That, paired with our wealth of experience and passion for growth, sets us apart from other private lenders.

All Deals Pre-Funded

All facilities are pre-funded, so the investment process is swift and simple.

Additional Security

Unlike many other private lending opportunities, Secured Lending may co-lend on the loans offered to Investor and will only be repaid once the Investor has been repaid in full.

Expertise

Our in-house team includes expertise across real property valuation, management and development, as well as finance experience gained in Top Four Accounting Firms, Global Banks, Private Equity and Listed Hedge Funds.

Stable Returns for Low Risk

We are able to provide attractive rates of return for low-risk contributions against secure first mortgage assets.

Recent loans

$800K Bridging Finance for Simultaneous Property Transactions in 48 Hours

$300K Second Mortgage for Dental Practice Working Capital in 5 Days

$700K Working Capital for a Technology Start-Up Settled in 72 Hours

$3M Working Capital for IT Business Expansion Settled in 2 Business Days

$1.9M Commercial Property Acquisition for Growing Doggy Daycare Business

$1.15M ATO Debt Cleared in 4 Business Days for Prahran Pub Operator

$250K Working Capital for Brisbane Café in 36 Hours

Case Study: Bridging the Payment Gap – How a Short-Term BLOC Saved a Commercial Builder's Project

See the full detail in the IM

The Information Memorandum covers the fund’s structure, target returns, security, fees and risks in full. Enter your details to download it.

First mortgage income FAQs

Common questions about first mortgage income and how the SL Premium Income Fund is secured.

Contact us

Learn more about mortgage fund investing

In-depth guides on how these funds are structured, secured and managed.

How private mortgage funds work, what drives return and risk, and how to assess a manager.

Why first-ranking security and the LVR buffer protect your capital, and what happens on default.

Pooled versus contributory, where pooling spreads risk, and where it stops.

Important Notice: This page contains general information only and is not financial advice. The SL Premium Income Fund is available to Wholesale and Sophisticated Investors only within the meaning of the Corporations Act 2001 and is not suitable for retail clients. The fund is issued by SL Premium Income Fund Pty Limited (ACN 664 382 076, AFSL 549857), as trustee. Target returns are not guaranteed, past performance is not indicative of future returns, and investments involve risk including the possible loss of capital. Read the Information Memorandum in full and seek independent advice before investing.