Private mortgage funds have moved from a niche corner of the market to a mainstream way for qualified investors to earn income. The reason is simple. Banks have pulled back from parts of property lending, and the funding gap has been filled by non-bank lenders backed by private capital. If you are weighing one of these funds, the questions that matter are not the marketing claims. They are structural: how the money is secured, who can invest, what drives the return, and how the manager behaves when a loan goes bad.

This guide explains how private mortgage funds work in Australia, what separates a well-run fund from a poorly run one, and the specific features you should understand before you commit. Our own SL Premium Income Fund gives wholesale and sophisticated investors access to private mortgage lending secured by first registered mortgages over Australian property, and we draw on it through this guide to show how the structure works in practice.

What is a private mortgage fund?

A private mortgage fund pools or directs investor money into loans that are secured by mortgages over real property. You are not buying property. You are stepping into the position of the lender. The borrower pays interest, and that interest, less the manager's fees and costs, flows back to you as income.

The structure is usually a unit trust. You buy units, the trust holds the loans and the mortgage security, and you hold a beneficial interest in the income and capital of the trust. The appeal is the combination of regular income and real-property security. The risk is that the borrower defaults and the security does not fully cover what is owed.

That trade-off, income now against the risk of loss later, is the entire game. Everything else in this guide is about understanding how a given fund manages it.

How the money actually flows

Understanding the mechanics protects you, so here is the full chain, using our own model as a worked example.

A borrower needs finance secured against property. The manager assesses the loan, the borrower, and the security. If approved, the loan settles and a mortgage is registered over the property. Investor capital funds the loan, and the borrower's interest payments become investor income, paid monthly or on whatever frequency the fund specifies.

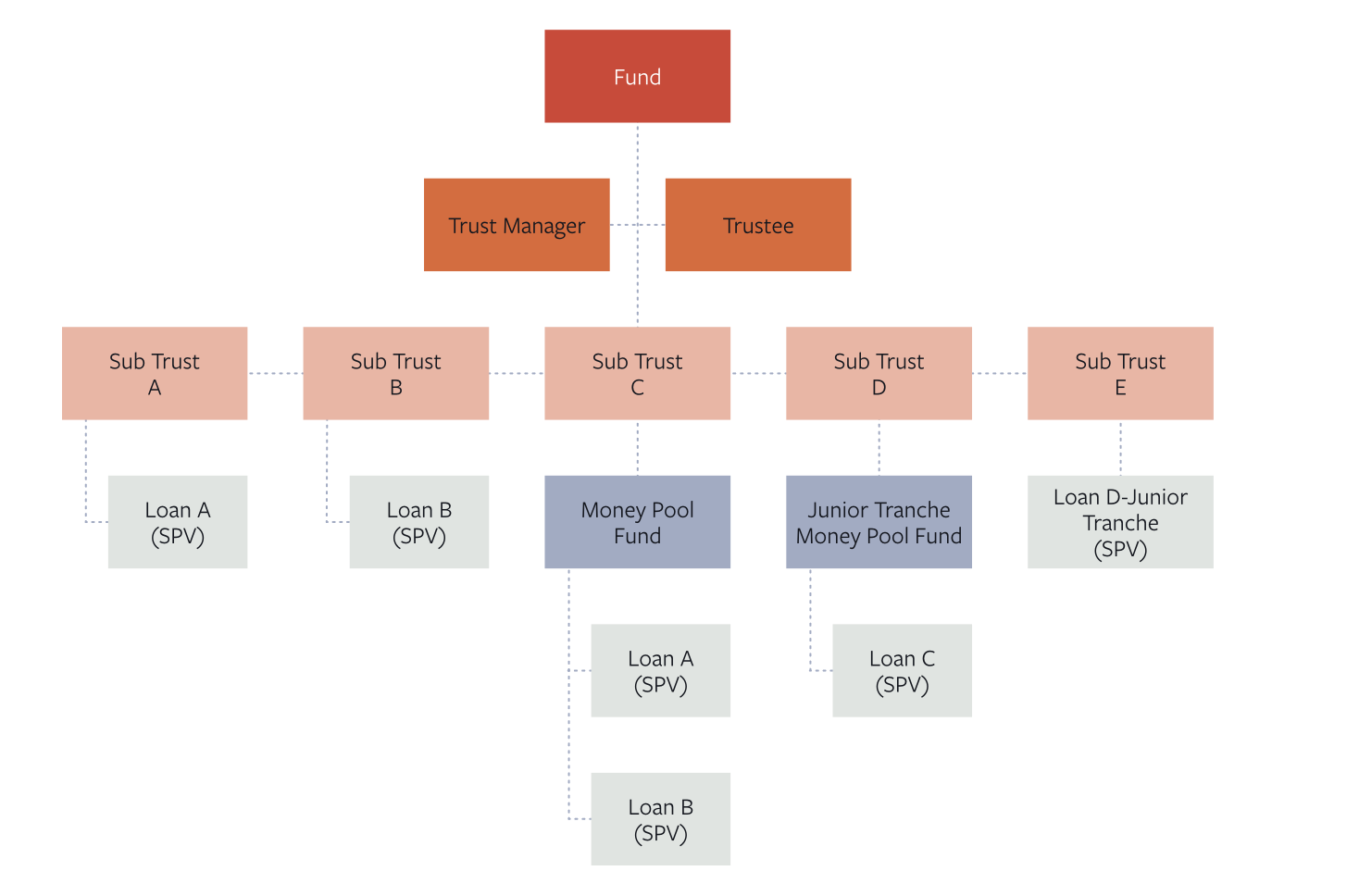

Funds differ in the sequence. In our SL Premium Income Fund, we use a pre-funded model. We settle each loan first using our own funds, which lets us fund within 24 hours, then assign the loan and its associated rights to the trustee under a separate Deed of Assignment and Transfer of Mortgage. Once assigned, the loan is held by the trustee for the benefit of the relevant sub-trust, and investors participate from that point. The practical effect is that the deal is already settled and secured before investor money is committed to it.

The unit pricing is usually fixed in these funds rather than marked to market daily. In our SL Premium Income Fund, each unit is priced at $1.00. Your return comes from income distributions, not from a rising unit price.

Contributory versus pooled: the structural choice

Within private mortgage funds there are two broad structures, and the difference changes your risk profile.

In a contributory structure, you choose the specific loan or sub-trust you invest in. You see the security, the loan-to-value ratio, the borrower profile, and the term, and you decide. You get transparency and control. The cost is effort and concentration, because your money may sit in a single loan.

In a pooled structure, your money sits across many loans and you receive a share of the blended income. You give up the ability to pick individual deals. In return you get diversification across the loan book and less work. The cost is reduced transparency and reliance on the manager's allocation.

Some managers offer only one model. We offer both. Our SL Premium Income Fund is structured with multiple sub-trusts and also includes a "Money Pool Fund" sub-trust, which allocates an investor's capital at our discretion across some or all of the sub-trusts. That means you can take a contributory approach by selecting a specific sub-trust, or a pooled approach through the Money Pool Fund. One caveat applies to the pooled option, and we state it plainly: we may allocate the entire amount to a single sub-trust, so the pooled option does not guarantee diversification in every case.

This guide covers the contributory and pooled choice in more depth in our pooled mortgage funds guide, and the importance of security ranking in our first mortgage investment funds guide.

What drives the return and the risk

Five factors do most of the work in any private mortgage fund. Learn to read them and you can assess almost any fund quickly.

Loan-to-value ratio. The LVR is the loan divided by the property value. A lower LVR means a bigger equity buffer beneath your loan, so prices have further to fall before your capital is at risk. Our standards generally cap LVR at 70 percent, measured on an "as is" basis for standing property and an "as if complete" basis for construction, though this varies by sub-trust.

Security ranking. A first mortgage ranks ahead of a second mortgage. If the property is sold under enforcement, the first mortgagee is paid before the second. First-ranking security is the single most important protection in this asset class. Our loans are secured by first registered mortgages.

Loan term. Shorter terms reduce the time your capital is exposed to a given borrower and give the manager more frequent decision points. We target loan terms generally under 12 months.

Borrower and purpose. These are commercial loans for business or investment purposes, not consumer loans, so they fall outside the National Consumer Credit Protection. Our standards set a minimum loan size of $250,000 and exclude consumer lending, loans to self-managed super funds as borrowers, and loans to non-residents.

Property type. Residential, commercial, industrial, vacant land, and part-complete development sites each carry different liquidity and recovery characteristics. Construction and development exposure carries more risk than a completed, income-producing building.

On returns, our SL Premium Income Fund targets 7 to 9.95 percent per annum, with the exact target varying by sub-trust. Treat that as a target, not a promise. There is no guarantee any sub-trust will achieve its target return, and no guarantee of capital.

The risks to understand

Real-property security reduces risk. It does not remove it. Our Information Memorandum sets out a full risk schedule, and the most important risks for an investor are these.

Credit and default risk. A borrower may default and the security may not cover the full amount owed. This is the central risk in the asset class.

Liquidity risk. These funds are illiquid. There is no secondary market for the units. Withdrawals are processed on the fund's terms, not on demand. In our SL Premium Income Fund, withdrawals are processed quarterly on the first business day of each calendar quarter, after a minimum holding period, with at least 30 business days' notice, and a minimum withdrawal of $100,000. Early redemption before the minimum holding period carries a fee of 2 percent and is at our discretion. Treat this as a fixed-term commitment, not an at-call account.

Market and valuation risk. A downturn in property values erodes the equity buffer beneath every loan. If a valuation was too high, the amount recovered on a forced sale may not cover the loan. Valuation discipline is therefore not a back-office detail. It is core to capital protection.

Construction and development risk. Where a fund lends against assets under construction, delays, cost overruns, or builder insolvency can reduce or delay income and impair recovery.

Concentration risk. A fund focused on property lending is not diversified across sectors, and some loans may be sizeable relative to the book. Pooling spreads single-loan risk but does not remove sector-wide or systematic risk.

Manager and operational risk. Your outcome depends heavily on the manager's judgement, processes, and conduct, and on the external parties it relies on, such as valuers and solicitors. If a fund's marketing emphasises the headline return and is quiet on these risks, that imbalance is itself information.

How to assess the manager

In a private mortgage fund you are not really buying a product. You are backing a manager's judgement. Four tests separate the serious operators, and here is how we measure up against each.

Track record, stated plainly and specifically. Look for real numbers on volume lent, number of loans, and capital losses, not vague claims. Since 2016 we have lent more than $500 million.

Recovery capability. The test of a lender is not how it behaves when loans perform. It is what happens when a loan fails. Ask who actually runs recovery. Ours is built for exactly this. Our team includes Mark Hutchins, our Managing Director, whose background spans insolvency practice, structured finance at a US-listed hedge fund, and bank workout; Daniel Juratowitch, a registered liquidator and bankruptcy trustee of more than 20 years and CEO of insolvency firm Cor Cordis; and Robert Rowlands, a registered valuer in New South Wales with more than 40 years of experience. A team that underwrites with the downside in mind, run by professionals who are called in when other lenders' loans fail, is structurally suited to this asset class.

Valuation discipline. Because recovery depends on the property's real value, the quality and independence of valuations is central. Ask who values security and how conservative the assumptions are. Our property security is assessed by a registered valuer, and our LVR caps are set against that assessment.

Alignment. Does the manager have its own capital at risk alongside yours? We settle loans with our own funds first under a pre-funded model, and where we co-lend, we are repaid only after the investor has been repaid in full. That alignment is a concrete structural feature, not a slogan, and it is worth confirming in the documents of any fund you consider.

The SL Premium Income Fund in brief

For wholesale and sophisticated investors, our SL Premium Income Fund provides access to first-mortgage-secured private lending. The detail below is summarised from its Information Memorandum dated 21 February 2024.

- •It is an unregistered managed investment scheme structured as a unit trust with multiple sub-trusts, including a Money Pool Fund for pooled exposure.

- •It is open to wholesale and sophisticated investors only. It is not available to retail clients, and it is not a PDS product.

- •The minimum investment is $100,000, with units priced at $1.00.

- •It targets a return of 7 to 9.95 percent per annum, varying by sub-trust, with no guarantee of return or capital.

- •Loans are secured by first registered mortgages over Australian real property, generally at up to 70 percent LVR, with target terms generally under 12 months.

- •The trustee is SL Premium Income Fund Pty Limited (AFSL 549857) and the trust manager is SL Group Management Pty Limited.

FAQs

What is a private mortgage fund?

It is an investment that lends your money to borrowers, secured by mortgages over real property. You earn income from the interest the borrowers pay. You are acting as a lender, not buying property.

Are private mortgage funds safe?

They are secured by real property, which reduces risk, but they are not guaranteed and not risk-free. The main risks are borrower default, illiquidity, and falling property values. First-ranking security and a conservative LVR are the features that protect capital most.

Who can invest in a private mortgage fund in Australia?

Some funds are registered and open to retail investors. Others, including our SL Premium Income Fund, are open only to wholesale and sophisticated investors, meaning you generally need to invest at least $500,000, or hold a qualified accountant's certificate confirming net assets of at least $2.5 million or income of at least $250,000 for the last two financial years, or be a professional investor.

What returns do private mortgage funds target?

Returns vary with risk. Our SL Premium Income Fund targets 7 to 9.95 percent per annum depending on the sub-trust, expressed as a target with no guarantee.

What is the difference between a registered and an unregistered fund?

A registered fund is registered with ASIC, issues a Product Disclosure Statement, and is subject to ASIC's RG 45 disclosure benchmarks for retail investors. An unregistered fund does neither and is restricted to wholesale and sophisticated investors, who carry more of the diligence burden themselves.

How do I get my money out?

These funds are illiquid with no secondary market. Withdrawals follow the fund's process. In our SL Premium Income Fund they are processed quarterly, after a minimum holding period, with at least 30 business days' notice and a minimum withdrawal of $100,000.

Invest with the SL Premium Income Fund

For wholesale and sophisticated investors, our private mortgage investment fund, the SL Premium Income Fund, puts these principles into practice. You can read more about the first mortgage income that secures every loan, or how the fund gives you exposure to alternative real estate debt.

This guide is general information only. It is not financial, tax, or legal advice, and it does not take account of your objectives, financial situation, or needs. Information about the SL Premium Income Fund is summarised from its Information Memorandum dated 21 February 2024; read the Information Memorandum in full for the complete terms. The Fund is open to wholesale and sophisticated investors only and is not a retail offer. Past performance is not a reliable indicator of future performance, and no return or capital is guaranteed. Seek independent professional advice before making any investment decision.