The entire value of a first mortgage is its position in the queue. When a property is sold to recover a bad loan, the first mortgagee is paid before anyone else with a claim against that property. That priority, combined with a disciplined loan-to-value ratio, is what protects an investor's capital. Everything else in a first mortgage investment fund follows from it.

This guide explains how first mortgage investment funds work in Australia, why security ranking matters so much, what happens when a loan defaults, and what to check before you commit. Our own SL Premium Income Fund provides wholesale and sophisticated investors with first mortgage investment opportunities, secured by first registered mortgages over Australian property, and we draw on it through this guide to show how these funds work in practice.

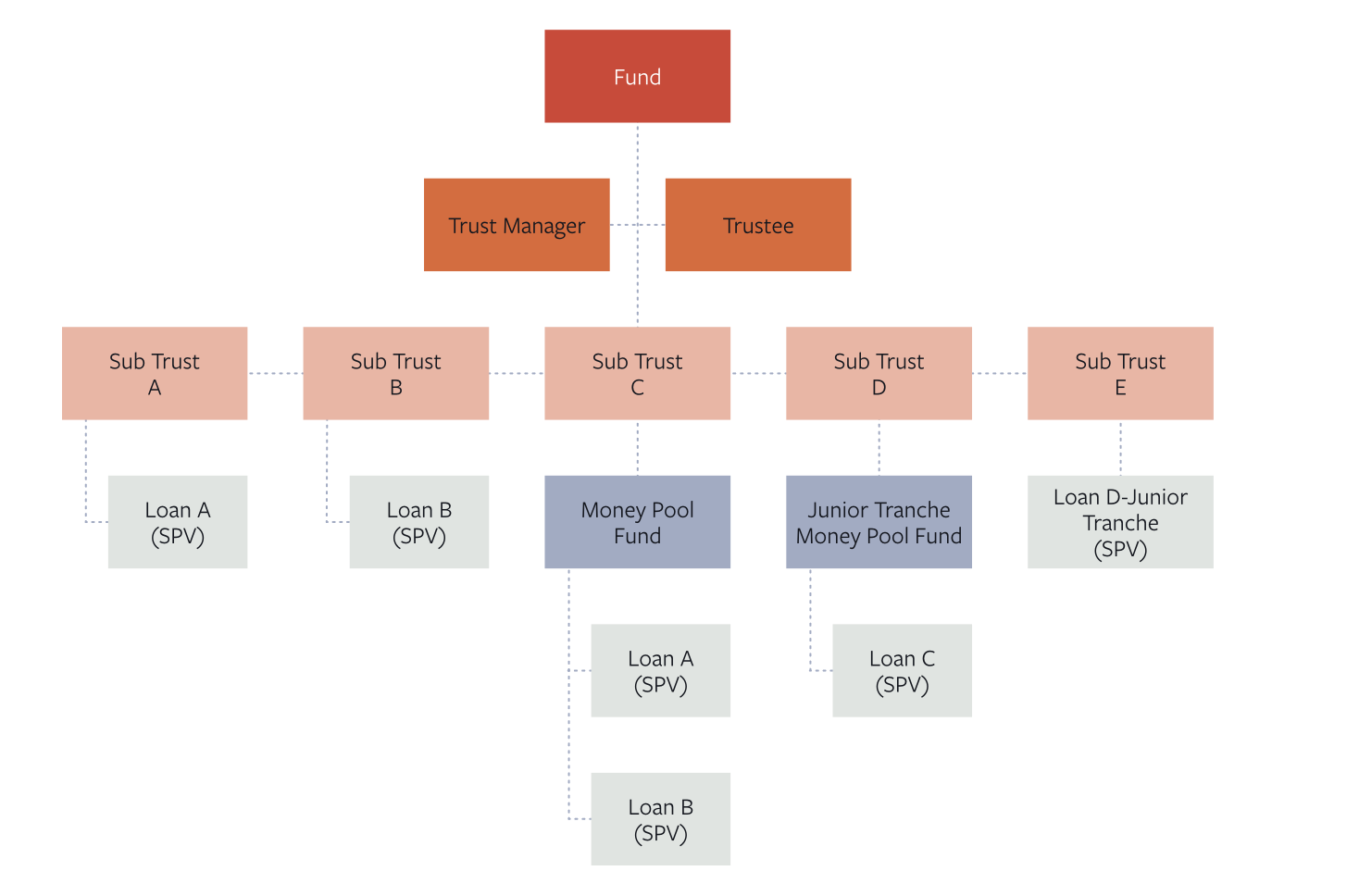

What is a first mortgage investment fund?

A first mortgage investment fund lends investor money to borrowers, secured by a first-ranking registered mortgage over real property. You are the lender. The borrower pays interest, and that interest, less the manager's fees and costs, is paid to you as income.

The defining feature is in the name. The fund holds a first mortgage, not a second or a lower-ranking interest. If the borrower fails and the property must be sold, the fund's claim sits at the front of the line. That single fact is the difference between this asset class and riskier forms of property lending.

The structure is usually a unit trust. You hold units, the trust holds the loans and the registered mortgages, and your return is income rather than capital growth. Unit prices are typically fixed. In our SL Premium Income Fund, for example, each unit is priced at $1.00.

Why first-ranking security is the priority

To understand a first mortgage, follow the money when a loan goes bad and the property is sold under enforcement. The sale proceeds are distributed in a strict order:

- •The costs of the sale and enforcement.

- •The first mortgagee, paid in full for principal, interest, and recoverable costs.

- •Any second or lower-ranking mortgagee, but only if money remains.

- •The borrower, only if anything is left after all the above.

A first mortgage investment fund holds position two. A second mortgage fund holds position three, and is exposed to a total loss before the first mortgagee loses a dollar. This is why first-ranking security is the strongest protection available in property lending, and why a higher yield on a second mortgage is not a free lunch. It is payment for standing further back in the queue.

The short version is that ranking determines who absorbs the loss first, and a first mortgage fund is structured so that you are not that party.

The LVR buffer explained

Security ranking tells you where you stand. The loan-to-value ratio tells you how much cushion sits beneath you. The LVR is the loan amount divided by the property's value.

Consider an illustrative loan of $700,000 against a property valued at $1,000,000. That is a 70 percent LVR. The borrower's equity, the $300,000 below the loan, is the buffer. Property values would need to fall by more than 30 percent, before sale costs, before the loan principal itself is exposed. The lower the LVR, the larger that buffer, and the more a market has to move against you before your capital is at risk.

Our loan standards generally cap LVR at 70 percent, measured on an "as is" basis for standing property and an "as if complete" basis for construction, with the exact limit varying by sub-trust. The value we use is based on advice from our property consultant, which is why valuation discipline matters so much. A buffer calculated from an inflated valuation is not a real buffer.

What "registered" actually gives you

The word registered carries legal weight, and it is worth understanding what it secures.

Australian land titles operate on the Torrens system, a government register of interests in land. When a mortgage is registered on the title, the lender's interest is recorded on that register. Registration gives the mortgagee a recognised, enforceable, priority interest in the property and access to the statutory power of sale. An unregistered or merely equitable mortgage is weaker, harder to enforce, and lower in priority. The difference becomes decisive in exactly the moment that matters, when a loan defaults and recovery begins.

Our loans are secured by registered first mortgages held in the name of the trust manager or a related party, equitably for the benefit of the trustee, and then assigned to the trustee. That security may be supported by additional protections, including guarantees from the directors of corporate borrowers, corporate guarantees from related third parties, and general or specific security over a borrower's assets registered on the Personal Property Securities Register. These are layers stacked on top of the first mortgage, not substitutes for it.

Returns and loan term

Returns in first mortgage funds reflect the risk taken. Our SL Premium Income Fund targets a return of 7 to 9.95 percent per annum, varying by sub-trust.

Loan terms shape risk as much as rate. Shorter terms reduce the time your capital is exposed to any single borrower and give the manager more frequent points to reassess. We target loan terms generally under 12 months, with a minimum loan size of $250,000. These are commercial loans for business or investment purposes, which places them outside the National Consumer Credit Protection regime.

Income frequency depends on the fund and sub-trust. The objective of this asset class is regular income from interest, not a capital gain on exit.

What happens when a borrower defaults

A first mortgage is only as good as the manager's ability to enforce it. This is the part of the process that separates serious operators from the rest, so it is worth knowing how recovery runs.

Our default process works as follows. If a default continues for more than seven days, we issue a default notice and follow our internal collection procedure. Where we consider it necessary in investors' interests, recovery action may include taking possession of and selling the property security, enforcing the security, appointing receivers, managing the property until a sale completes, and taking legal action against borrowers and guarantors.

We are also direct about the limits. During a default, distributions may be delayed or may not occur while recovery proceeds. Additional costs may be incurred. If the amount recovered after mortgagee possession is lower than the loan principal, the available funds are distributed to investors in the relevant sub-trust on a pro-rata basis. We do not guarantee full recovery of principal. A first mortgage strongly improves your position in recovery. It does not make you immune to loss.

The risks specific to first mortgage funds

First-ranking security and a conservative LVR reduce risk. They do not remove it. The risks that matter most in this asset class are these.

Valuation risk. Your buffer is only as reliable as the valuation it is built on. If the assigned value of a security property is too high, the amount realised on a forced sale may not cover the loan. This is the risk that most directly undermines the LVR protection, which is why the independence and conservatism of valuations is central.

Credit and default risk. A borrower may fail and the security may fall short of the amount owed, particularly after enforcement costs.

Interest capitalisation risk. Where interest is capitalised rather than paid as it accrues, the total owed grows over the loan term. The proceeds of a sale in possession may then be lower than the full amount of principal plus capitalised interest.

Liquidity risk. These funds are illiquid, with no secondary market for units. Withdrawals run on the fund's terms. In our SL Premium Income Fund, withdrawals are processed quarterly on the first business day of each calendar quarter, after a minimum holding period, with at least 30 business days' notice and a minimum of $100,000. Early redemption before the minimum holding period carries a 2 percent fee and is at our discretion. Treat the investment as a fixed-term commitment.

Construction and development risk. Where a loan funds a property under construction, delays, cost overruns, or builder insolvency can impair both income and recovery.

Concentration risk. A fund focused on first mortgages over property is not diversified across asset classes, and individual loans can be significant relative to the book.

How to assess a first mortgage fund manager

In a first mortgage fund you are backing the manager's judgement: their underwriting, their valuation discipline, and above all their ability to recover. Four checks matter most, and here is how we measure up against each.

Recovery capability. A lender is tested when a loan fails, not when it performs. Ask who actually runs recovery and what their background is. Ours is built for it. Our team includes Mark Hutchins, our Managing Director, whose background spans insolvency practice, structured finance at a US-listed hedge fund, and bank workout; Daniel Juratowitch, a registered liquidator and bankruptcy trustee of more than 20 years and CEO of insolvency firm Cor Cordis; and Robert Rowlands, a registered valuer in New South Wales with more than 40 years of experience. A first mortgage is a recovery instrument, and a team drawn from insolvency and valuation is built to use it.

Valuation discipline. Because the LVR buffer depends entirely on the property's real value, ask who values the security, whether they are independent and licensed, and how conservative the assumptions are. Our security is assessed by a registered valuer, and our LVR caps are set against that assessment.

Track record, with specifics. Look for volume lent, number of loans, and capital losses, not vague claims. Since 2016 we have lent more than $500 million.

Alignment. Does the manager have its own money at risk alongside yours? We settle loans with our own funds first under a pre-funded model, and where we co-lend, we are repaid only after the investor has been repaid in full.

The SL Premium Income Fund as a first mortgage fund

For wholesale and sophisticated investors, our SL Premium Income Fund provides first-mortgage-secured investment. The detail below is summarised from its Information Memorandum dated 21 February 2024.

- •Loans are secured by first registered mortgages over Australian real property, generally at up to 70 percent LVR.

- •Target loan terms are generally under 12 months, with a minimum loan size of $250,000.

- •The fund targets 7 to 9.95 percent per annum, varying by sub-trust, with no guarantee of return or capital.

- •It is an unregistered managed investment scheme, structured as a unit trust with multiple sub-trusts. It is not a PDS product.

- •It is open to wholesale and sophisticated investors only, and is not available to retail clients.

- •The minimum investment is $100,000, with units priced at $1.00.

- •The trustee is SL Premium Income Fund Pty Limited (AFSL 549857) and the trust manager is SL Group Management Pty Limited.

FAQs

What is a first mortgage investment fund?

A fund that lends investor money to borrowers, secured by a first-ranking registered mortgage over real property. You earn income from the interest. The first mortgage gives you priority of repayment if the property must be sold.

How is a first mortgage different from a second mortgage for an investor?

A first mortgage is repaid before a second when a property is sold under enforcement. A second mortgage carries a higher yield because it stands behind the first and absorbs losses earlier. The extra return is compensation for the weaker position.

What LVR is considered safe?

A lower LVR means a larger equity buffer beneath the loan. Many conservative funds cap LVR around 70 percent, which means values would need to fall by more than 30 percent before the loan principal is exposed, before sale costs. Our SL Premium Income Fund generally caps LVR at 70 percent, varying by sub-trust.

What happens if a borrower defaults?

The manager enforces the security, which can include taking possession and selling the property, appointing receivers, and pursuing borrowers and guarantors. If the recovery falls short of the principal, the shortfall is shared by investors in the relevant sub-trust. A first mortgage improves recovery but does not guarantee full repayment.

What returns do first mortgage funds target?

Returns reflect risk. Our SL Premium Income Fund targets 7 to 9.95 percent per annum depending on the sub-trust, expressed as a target with no guarantee.

Who can invest in a first mortgage fund in Australia?

Some funds are registered and open to retail investors. Others, including our SL Premium Income Fund, are open only to wholesale and sophisticated investors, which generally means investing at least $500,000, or holding a qualified accountant's certificate confirming net assets of at least $2.5 million or income of at least $250,000 for the last two financial years, or being a professional investor.

Invest with the SL Premium Income Fund

For wholesale and sophisticated investors, our first mortgage income fund secures every loan at the front of the repayment queue. You can also explore the broader private mortgage investment fund and how it gives investors exposure to alternative real estate debt.

This guide is general information only. It is not financial, tax, or legal advice, and it does not take account of your objectives, financial situation, or needs. Information about the SL Premium Income Fund is summarised from its Information Memorandum dated 21 February 2024; read the Information Memorandum in full for the complete terms. The Fund is open to wholesale and sophisticated investors only and is not a retail offer. Past performance is not a reliable indicator of future performance, and no return or capital is guaranteed. Seek independent professional advice before making any investment decision.