Fast, Strategic Finance Within 24 Hours

Australia's fastest private lender

Experts in complex lending and strategic, short-term finance

The Secured Lending Difference

Fast, flexible private lending solutions for Australian businesses and investors.

We can provide funding within 24 hours of application.

Loans from $250k up to $10 million secured against property.

Competitive rates from 9.7% p.a depending on loan type and security.

Flexible short-term loan periods from 1 to 24 months.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.

Scenarios We Can Help With

Browse our full range of private lending scenarios we can help assist with.

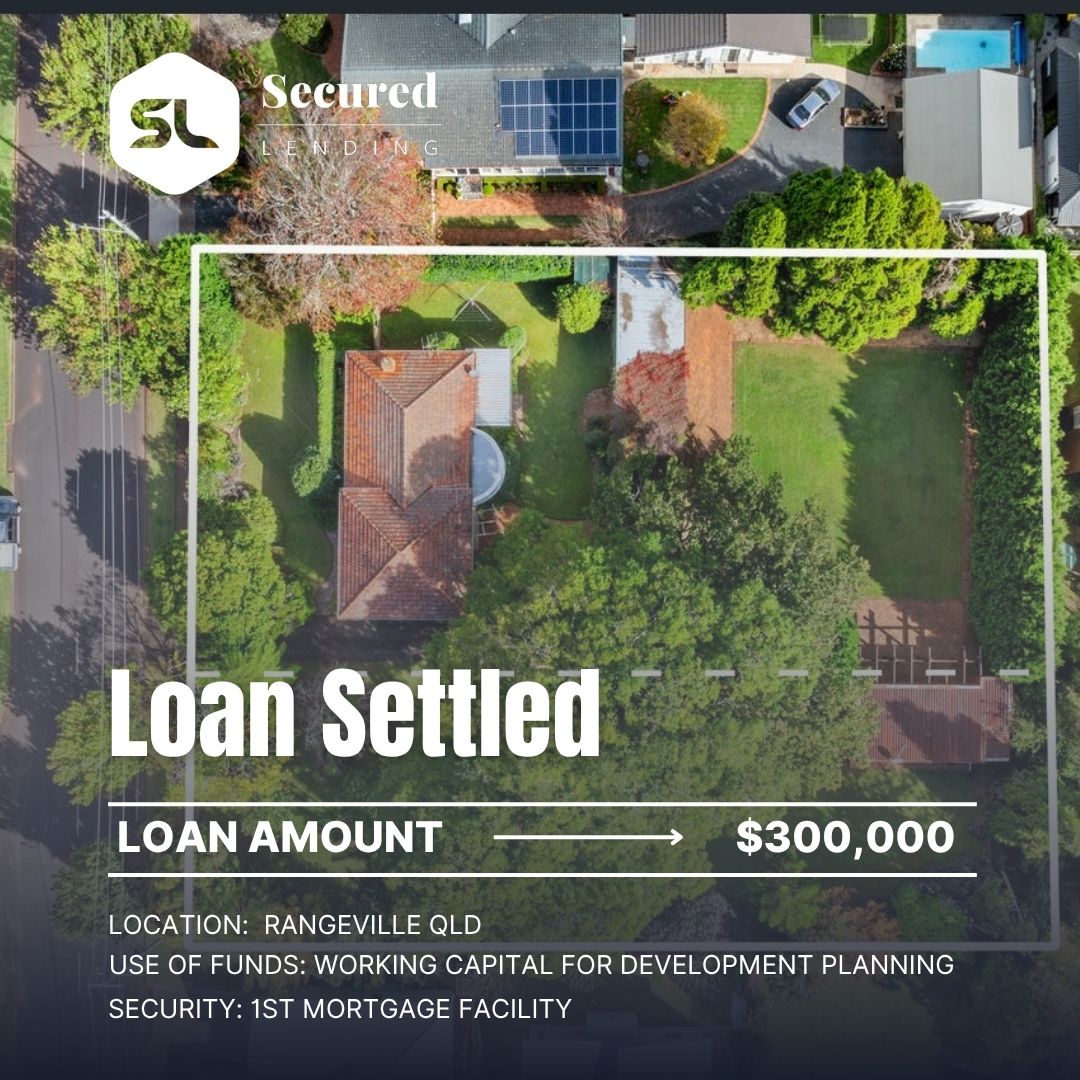

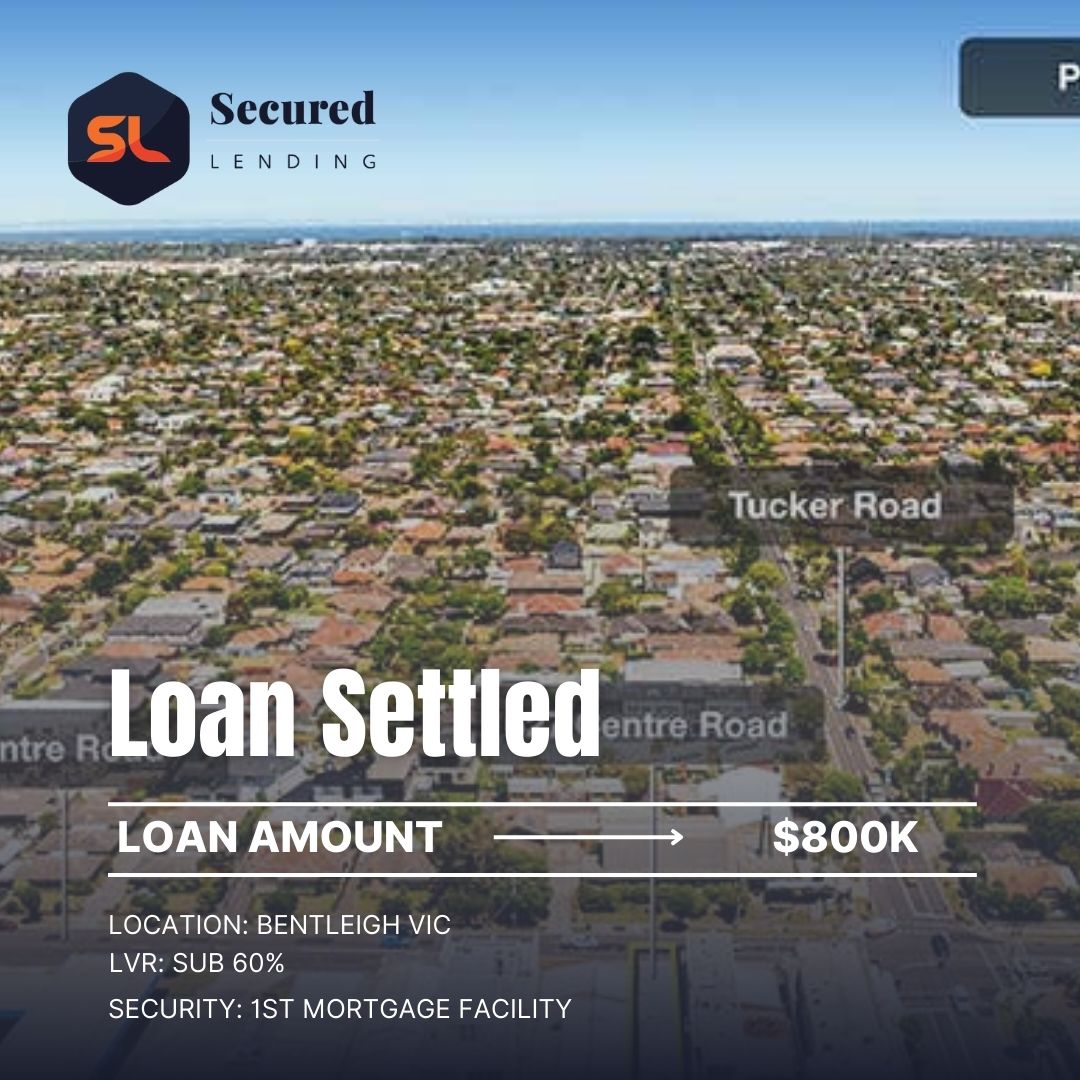

Case Studies

Australia's Fastest Private Lender

- •We are a private, non-bank lender

- •Leaders in strategic and short term finance within Australia

- •Funding in 24 hours

- •We use our own private funds

- •Internal property valuation team

- •Loans from $250,000 to $10 million

- •Over $500M loans facilitated