Commercial property refinancing to a private lender is not a permanent destination; it is a tactical step. When a bank facility expires and the bank will not renew, when credit policy has changed and the borrower no longer fits, or when an existing private loan is carrying rates or terms that need replacing, a refinance buys time. The private loan holds the asset while the borrower arranges a better long-term facility, resolves whatever triggered the bank's decision, or positions the property for sale.

Who This Is For

- •Borrowers whose bank has notified them the existing commercial facility will not be renewed at expiry

- •Borrowers who need to exit their current lender quickly due to a rate review, covenant breach, or relationship breakdown

- •Companies and trusts refinancing from another private lender to buy more time or access better terms

- •Borrowers who have had a bank decline a refinance application and need an immediate alternative

- •SMSFs needing to refinance an LRBA from a lender that is exiting that product segment

- •Not available to natural persons borrowing in their personal name

- •Not available for residential property or any NCCP-regulated consumer lending

How We Assess Commercial Property Refinances

Our refinance assessment centres on the current value of the commercial property, the refinance amount required, and the borrower's plan for the loan term. We require a current or recent valuation and will arrange our own in-house valuation if needed. The existing loan history is useful context but is not the primary credit input; the security property and the exit strategy are.

For refinances triggered by a bank non-renewal, we work quickly. A bank notifying it will not renew typically gives the borrower 30 to 90 days. That timeline is tight for organising a bank replacement, but comfortable for a private lending refinance that then gives the borrower 6 to 18 months to arrange the long-term solution. We discuss the exit strategy at application to set the term correctly.

Submit your scenario with the property details, the current loan amount, the reason for the refinance, and your intended exit from the private facility. Same-day indicative response. Letter of offer within 24 hours of agreed terms.

Three Commercial Refinance Scenarios We Have Recently Helped

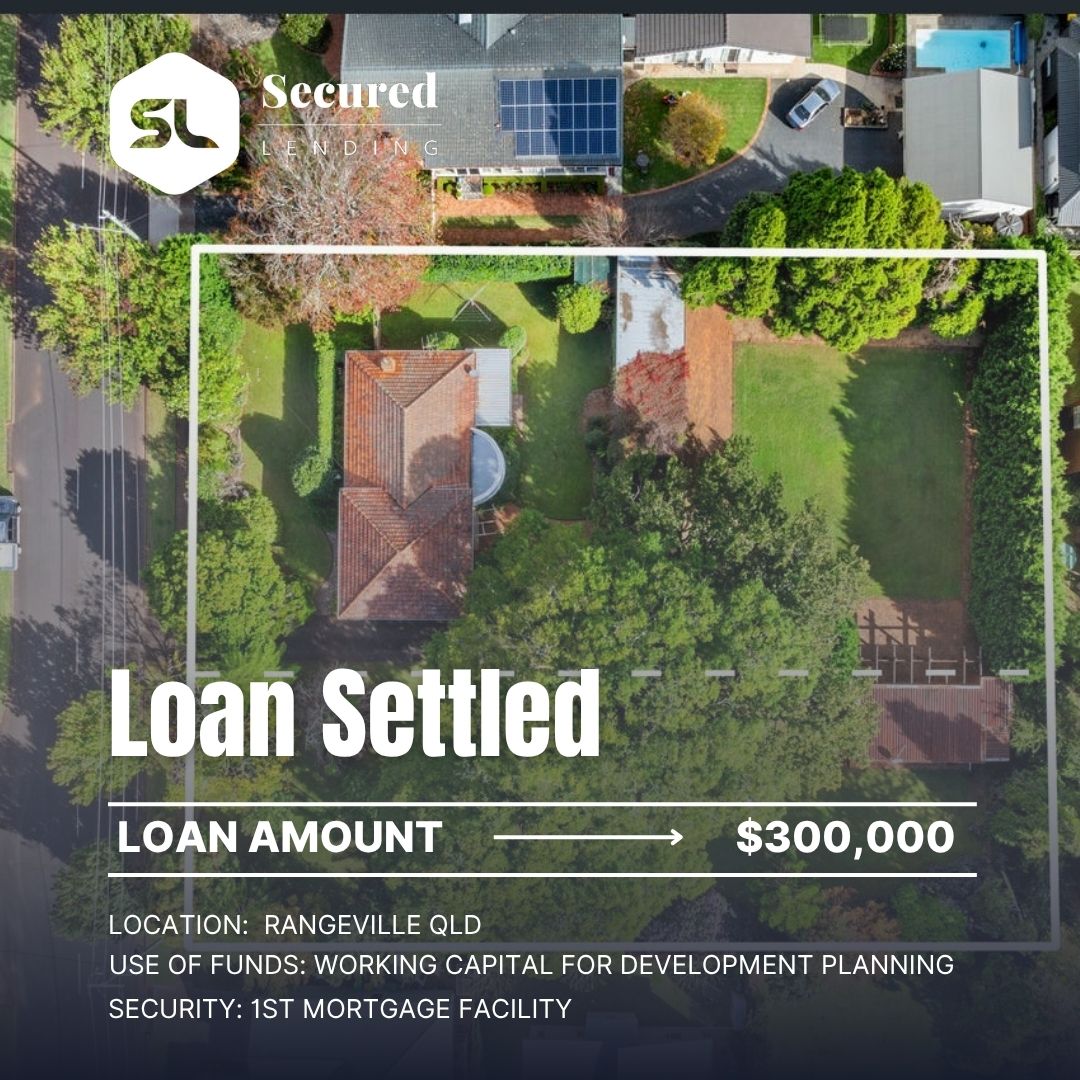

A family trust received a notice from its bank that its commercial property facility would not be renewed at the 3-year anniversary. The bank cited a portfolio exposure review rather than any performance issue with the trust's loan. The trust had 60 days. We refinanced the existing loan and gave the trust 18 months to identify and complete a permanent replacement facility. Loan: $3.2 million.

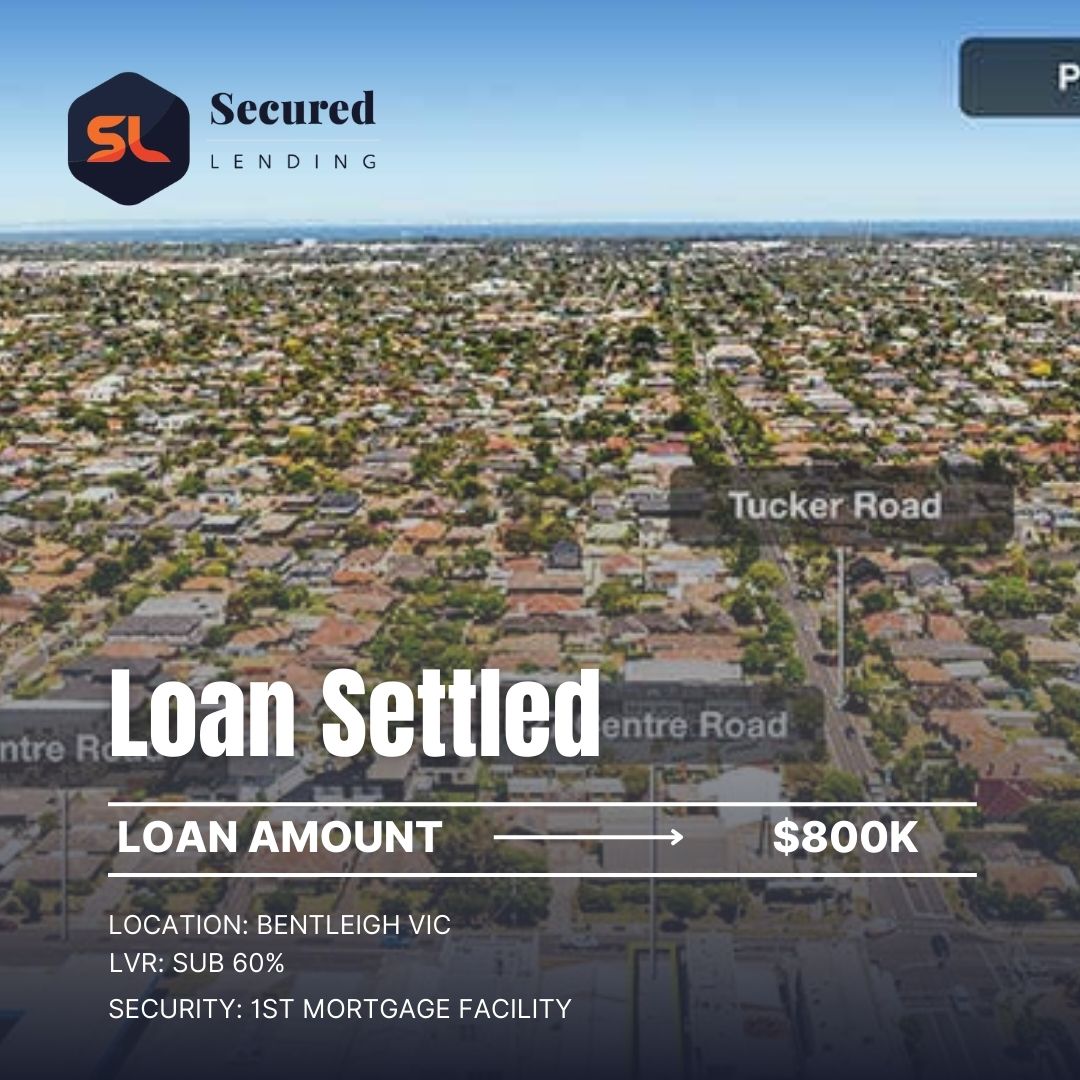

A Pty Ltd company had an existing private lender facility on a commercial investment property at a rate significantly above market. The company had improved its financial position since the original loan was taken and qualified for better terms. We refinanced the existing private lender out and provided a 12-month facility at a materially lower rate while the company completed its bank application. Loan: $1.8 million.

An SMSF's specialist LRBA lender announced it was exiting the commercial property LRBA market. The fund had 90 days to find a replacement lender. The fund's preferred bank needed 16 weeks. We refinanced the LRBA on a 12-month bridging basis under the same bare trust structure. The fund completed its bank LRBA during the term. Loan: $750,000.

Speed and Process Advantage

Commercial property refinance is time-sensitive by nature. A bank non-renewal notice sets a hard deadline, and finding a replacement on that timeline requires a lender that can move quickly. We hold direct credit authority with no external committee, run in-house valuations concurrently with underwriting, and can provide a letter of offer within 24 hours of agreed terms. For borrowers facing a non-renewal deadline, this speed is what makes the difference.

Related Commercial Property Finance

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.