Mainstream bank appetite for retail commercial property has become inconsistent. Certain retail categories, including food and beverage tenancies, fashion, stand-alone shopfronts, and secondary location retail strips, have seen reduced bank appetite regardless of the underlying asset quality. That creates a real problem for investors who understand retail property and can identify quality assets at appropriate prices. Private lending does not apply sector-level policy. Every retail deal is assessed on the asset, the LVR, and the exit.

Who This Is For

- •Pty Ltd companies purchasing retail premises for investment or owner-occupier use

- •Discretionary and unit family trusts acquiring retail property for yield

- •SMSFs purchasing retail commercial property under LRBA as qualifying business real property or investment

- •Retailers buying their own shopfront or showroom through a corporate structure

- •Investors acquiring retail strips, strata retail, or large-format assets where banks have pulled back

- •Not available to natural persons borrowing in their personal name

- •Not available for owner-occupier residential or any NCCP-regulated consumer credit

How We Assess Retail Property

Our assessment starts with the security property: its location, the improvements, the title, and the value our in-house valuers determine. Lease quality and tenant covenant inform our view of risk but do not replace the asset-first assessment. A well-located retail property with a short-dated tenancy or a vacancy period is still a quality asset if the fundamentals support it.

We do not apply blanket retail sector exclusions. A food and beverage tenancy that a bank's credit policy has categorised as high-risk is assessed by us on the specific property, location, and borrower. This is how we fund deals that move within the gap left by banks stepping back from retail.

Submit your scenario with property details, entity type, and proposed LVR. Same-day indicative response. Letter of offer within 24 hours of agreed terms. Settlement from 24 to 72 hours for clean deals.

Three Retail Property Scenarios We Have Recently Helped

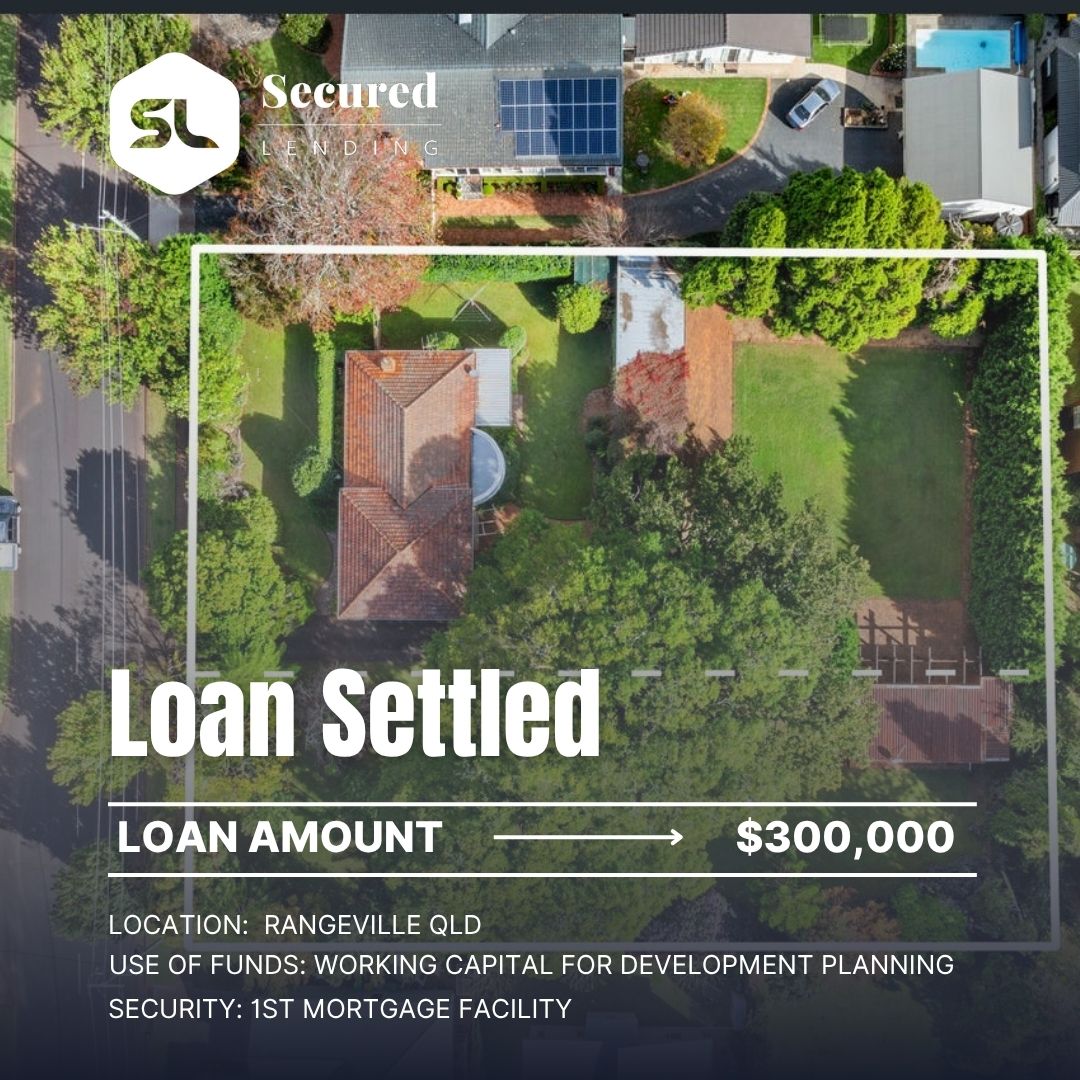

A family trust with a diversified commercial portfolio identified a strata retail unit in an inner Sydney suburb. The tenant was a national pharmacy chain on a four-year lease. The bank declined on entity structure complexity across the trust group. We assessed on asset quality and the lease covenant. Loan: $680,000, first mortgage, 61% LVR.

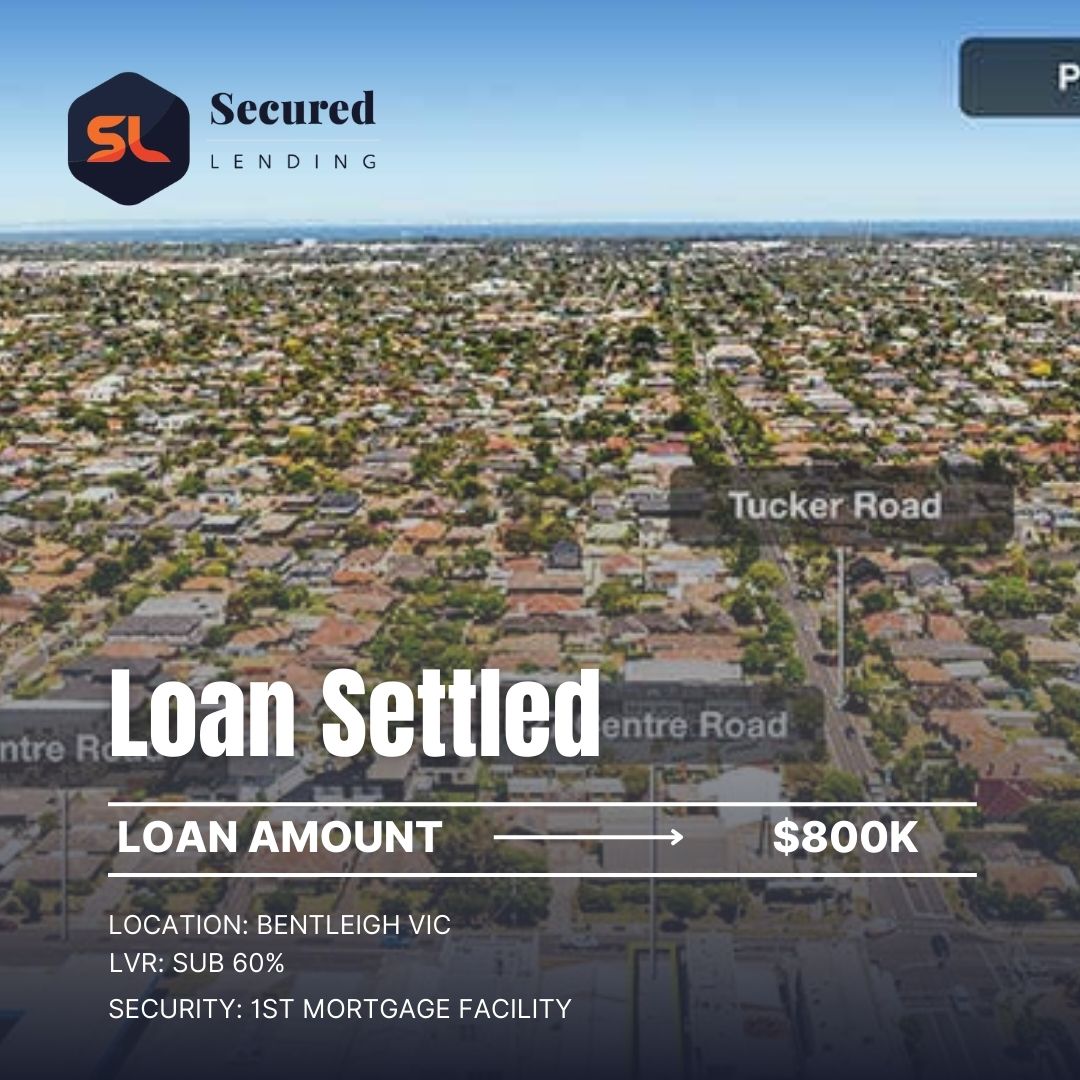

A Pty Ltd company operating a furniture showroom had leased its large-format retail premises for seven years. The landlord offered to sell. The company wanted to buy but its bank had a 12-week processing timeline and the vendor needed settlement in 45 days. We bridged the timing gap. Loan: $2.4 million, first mortgage, 63% LVR. The company refinanced to its bank at the end of a nine-month term.

A property investor operating through a family trust identified a retail strip property in a regional NSW coastal town. Multiple tenants across food, service, and convenience categories, strong occupancy history. The bank declined on a combination of location and retail sector exposure policy. We assessed the asset on its fundamentals. Loan: $1.7 million, first mortgage, 65% LVR.

Speed and Process Advantage

Direct credit authority, in-house valuation, and no external committee mean we can move faster than any bank on retail commercial property. For investors who have found a quality retail asset at the right price and cannot afford to lose it to a competitor with finance already in place, that speed is the competitive edge. Same-day assessment. Settlement from 24 hours where the deal is clean.

Related Commercial Property Finance

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.