Trust structures are among the most common holding vehicles for commercial property in Australia, and among the most misunderstood by bank credit teams. Discretionary trusts with multiple beneficiaries, related corporate trustees, and layered group structures often trigger policy restrictions at mainstream banks that have nothing to do with the quality of the underlying asset or the creditworthiness of the effective controller. Private lending assesses the security property and the trustee's capacity to hold and exit, rather than applying blanket trust-policy restrictions.

Who This Is For

- •Discretionary family trusts with a corporate trustee purchasing commercial investment or owner-occupier property

- •Unit trusts where unitholders are companies or other trusts, creating a structure banks find difficult to assess

- •Trusts purchasing commercial property in time-critical settlements where bank processing cannot keep pace

- •Trust borrowers who have been declined by a bank due to the trust deed, beneficiary complexity, or group structure

- •Trusts with an existing commercial portfolio seeking to add assets without waiting on bank serviceability modelling

- •Not available to bare trusts holding property under an SMSF LRBA (that lending falls under our SMSF product)

- •Not available for residential property or any NCCP-regulated consumer lending

How We Assess Trust Borrowers

Our assessment requires confirmation that the trust is properly constituted, that the trustee has capacity to borrow on behalf of the trust, and that the trust deed permits the relevant borrowing and security giving. We work with your solicitor to review the trust deed and confirm the structure before proceeding. This review runs concurrently with our property assessment rather than sequentially, which preserves time.

The credit decision centres on the security property and the exit. The trustee and beneficiary guarantors are assessed proportionately. For trusts with corporate trustees, the directors of the trustee company are typically required to guarantee. For trusts with individual trustees, the trustees guarantee directly. Neither case requires a perfect personal credit history across all parties.

Submit your scenario with the trust structure details, the security property, and the proposed LVR. Same-day indicative response. Letter of offer within 24 hours of agreed terms. Settlement from 24 to 72 hours for clean deals.

Three Trust Borrower Scenarios We Have Recently Helped

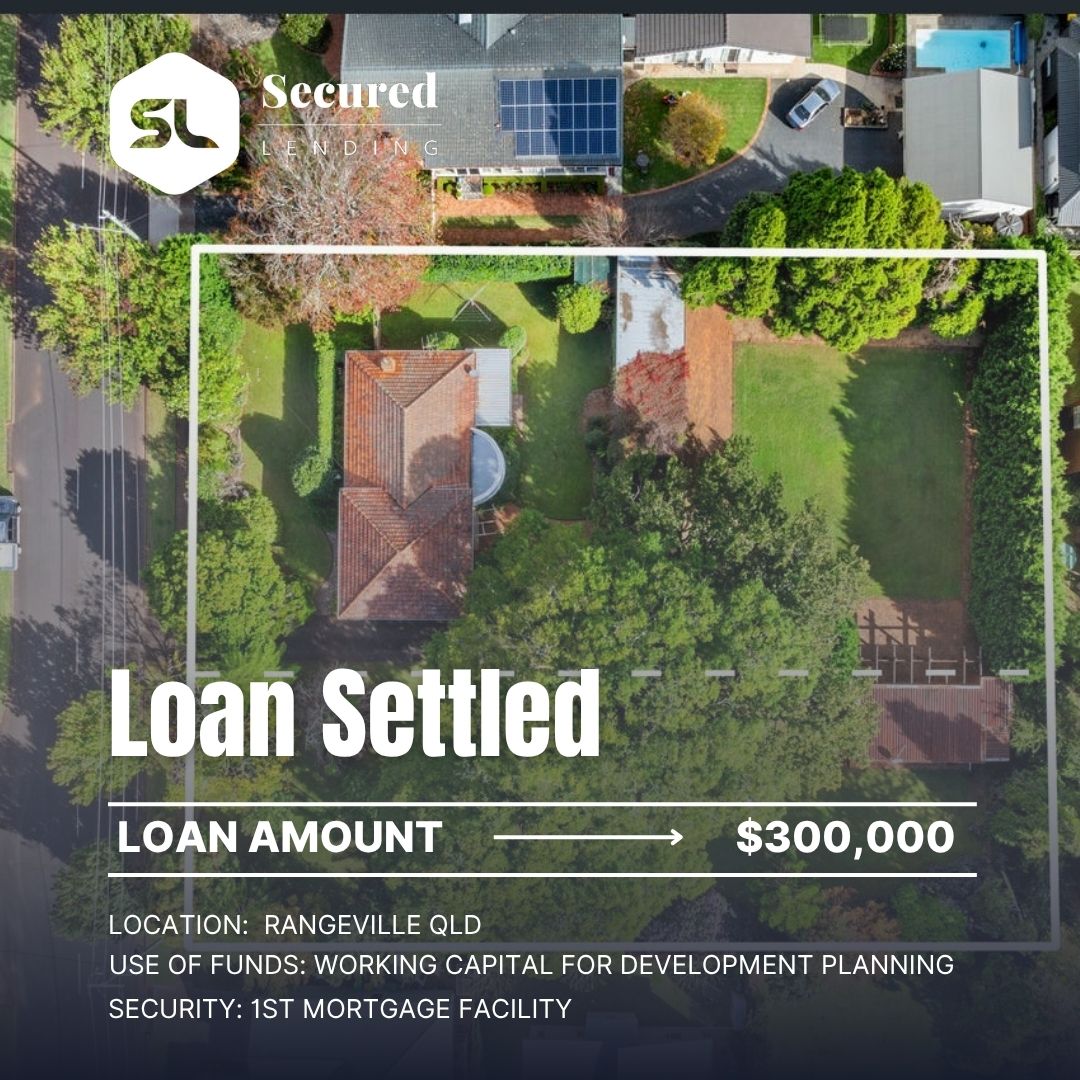

A discretionary family trust with a corporate trustee wanted to purchase a suburban retail property at an unconditional contract deadline of 21 days. The trust's bank required assessment of all group entities across three related trusts before it could proceed. We assessed the security property and the trustee company's capacity to proceed. Loan: $2.1 million, first mortgage, 65% LVR, 12-month term.

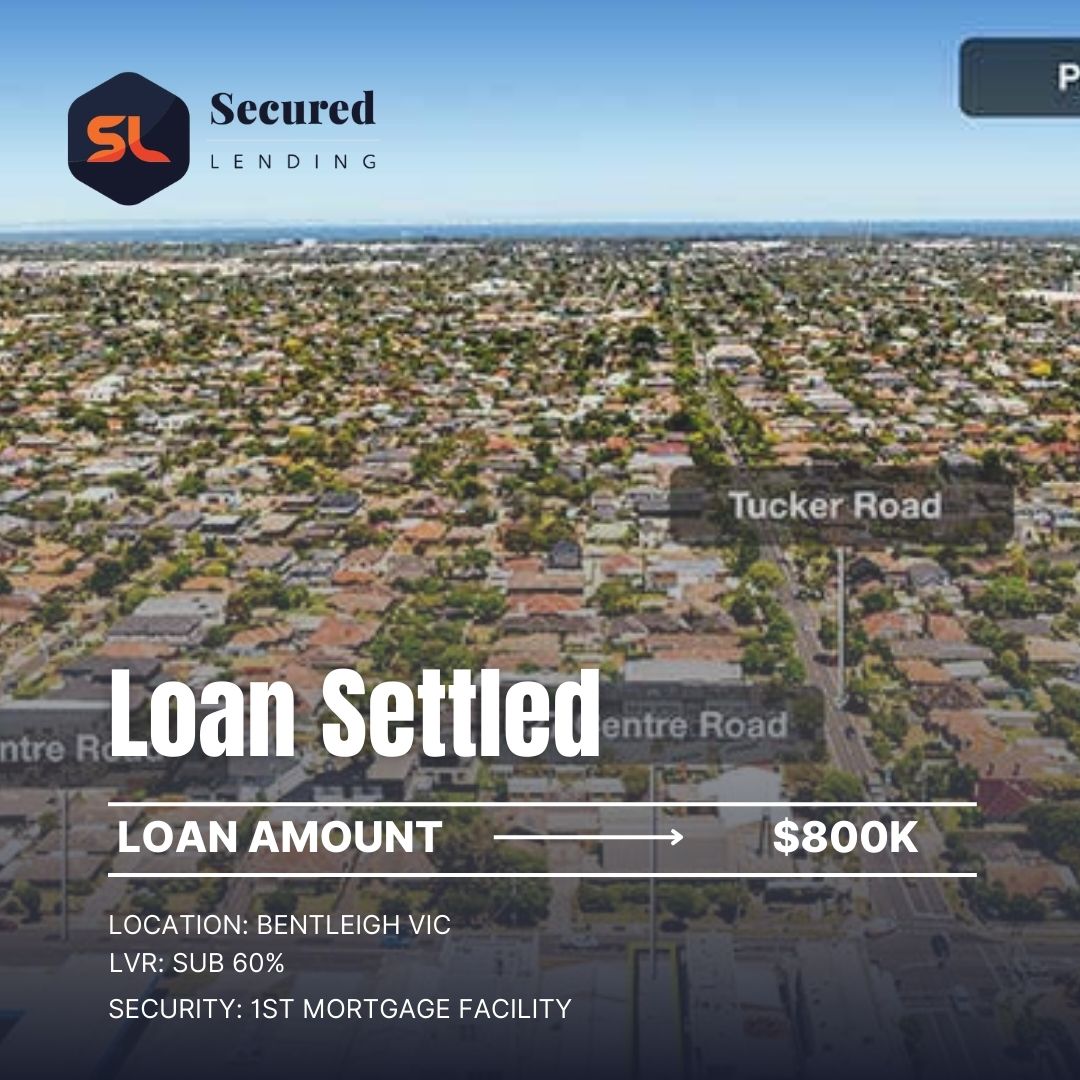

A unit trust with four corporate unitholders needed to refinance its existing commercial property loan after the bank notified it would not renew. The complex unitholder structure created a policy flag at two alternative banks. We assessed on the property value, the loan amount, and the trust's ability to service during the loan term. Loan: $3.8 million refinance, 18-month term to allow time for a bank refinance.

A family trust had been declined by its bank for a second commercial property purchase. The bank cited the trust's existing loan-to-income ratio across the whole portfolio. We assessed the new acquisition on its own merits: the property, the LVR, and the exit. The existing portfolio was not part of our assessment. Loan: $1.4 million, settled within 5 business days.

Speed and Process Advantage

We hold direct credit authority with no external committee. Trust deed review, property valuation, and underwriting run concurrently. For trust borrowers in time-critical purchase or refinance situations, we provide an indicative position the same day you submit a complete scenario and can settle within 24 to 72 hours for clean deals. Trust complexity is not a reason for a slower process with us.

Related Commercial Property Finance

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.