Holding residential investment property in a Pty Ltd company is a deliberate choice. It creates separation between personal assets and the investment portfolio, keeps exposure from crossing between business and personal balance sheets, and can suit certain tax and estate planning strategies. The problem is that banks treat company borrowers with far more friction than individual borrowers — particularly when the company is small, recently incorporated, or has revenue that does not fit a standard serviceability template.

Secured Lending assesses company investment property loans differently. We look at the security property, the LVR, the directors behind the company, and the exit strategy. For short-term facilities secured against well-located residential property, those factors matter more than three years of company financials.

Why Company Borrowers Hit Walls at Banks

Banks want income — ideally PAYG, two years minimum. A company that pays its director a modest salary and retains profits, or one that has had a strong recent year after a quiet period, often cannot satisfy a bank's debt serviceability test even when the equity position is solid. Add in a complex company structure, multiple directorships, or related entity cross-collateralisation, and the application stalls in credit assessment with no clear path forward.

A private lender does not use the same model. Our credit decision focuses on whether the security property supports the loan amount and whether there is a credible, documented exit. Director guarantees are standard. Trading history is contextual, not a hard filter.

Who This Is For

- •Pty Ltd companies purchasing residential investment property as a business-purpose transaction

- •Companies refinancing existing investment property loans — to exit arrears, restructure debt, or free equity

- •Business owners separating investment property from their personal balance sheet for asset protection

- •Companies needing to act quickly — auction purchases, settlement deadlines, or time-sensitive equity release

- •Not for owner-occupier purchases, personal use, or borrowing in personal name

How the Assessment Works

The company must be registered and in good standing with ASIC. Directors provide personal guarantees as a standard condition — this applies to all private and non-bank lenders for business-purpose lending. We review the security property and its location, the proposed LVR (our standard maximum is 70%), the purpose of the loan, and the proposed exit: refinance to a bank or non-bank, property sale, or internal repayment from business cash flow.

For most deals, we can give an indicative assessment on the day we receive a complete enquiry. A letter of offer follows quickly if we can proceed, and settlement is coordinated with your solicitor from there.

Three Deals We Have Done

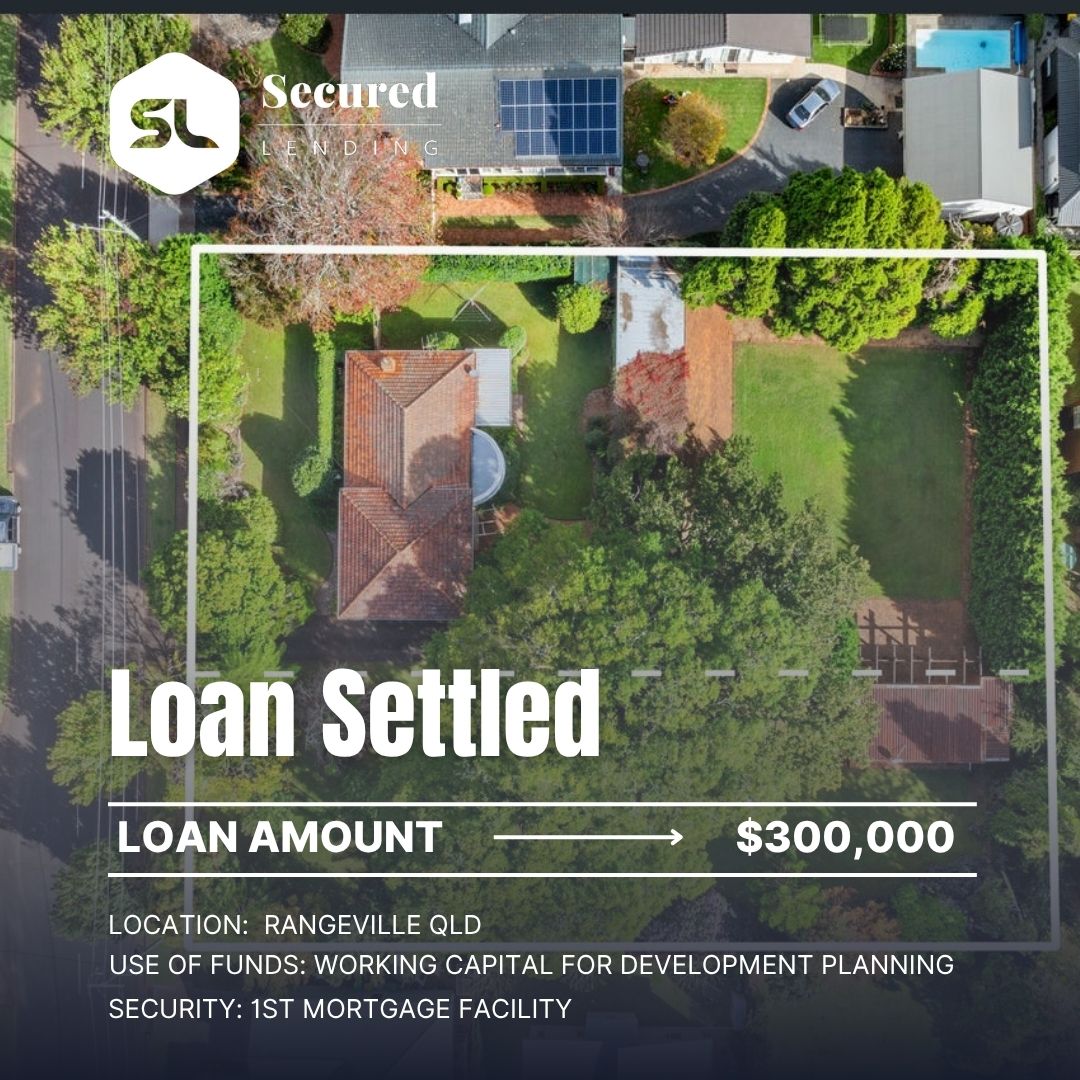

A construction company director in western Sydney wanted to purchase a $1.65M residential investment property through the company rather than personally. His bank declined the company application, citing variable revenue from project-based work. We assessed on the property location and condition, the director's personal guarantee, and a 12-month term with exit via refinance to a specialist non-bank lender. Settled in 48 hours.

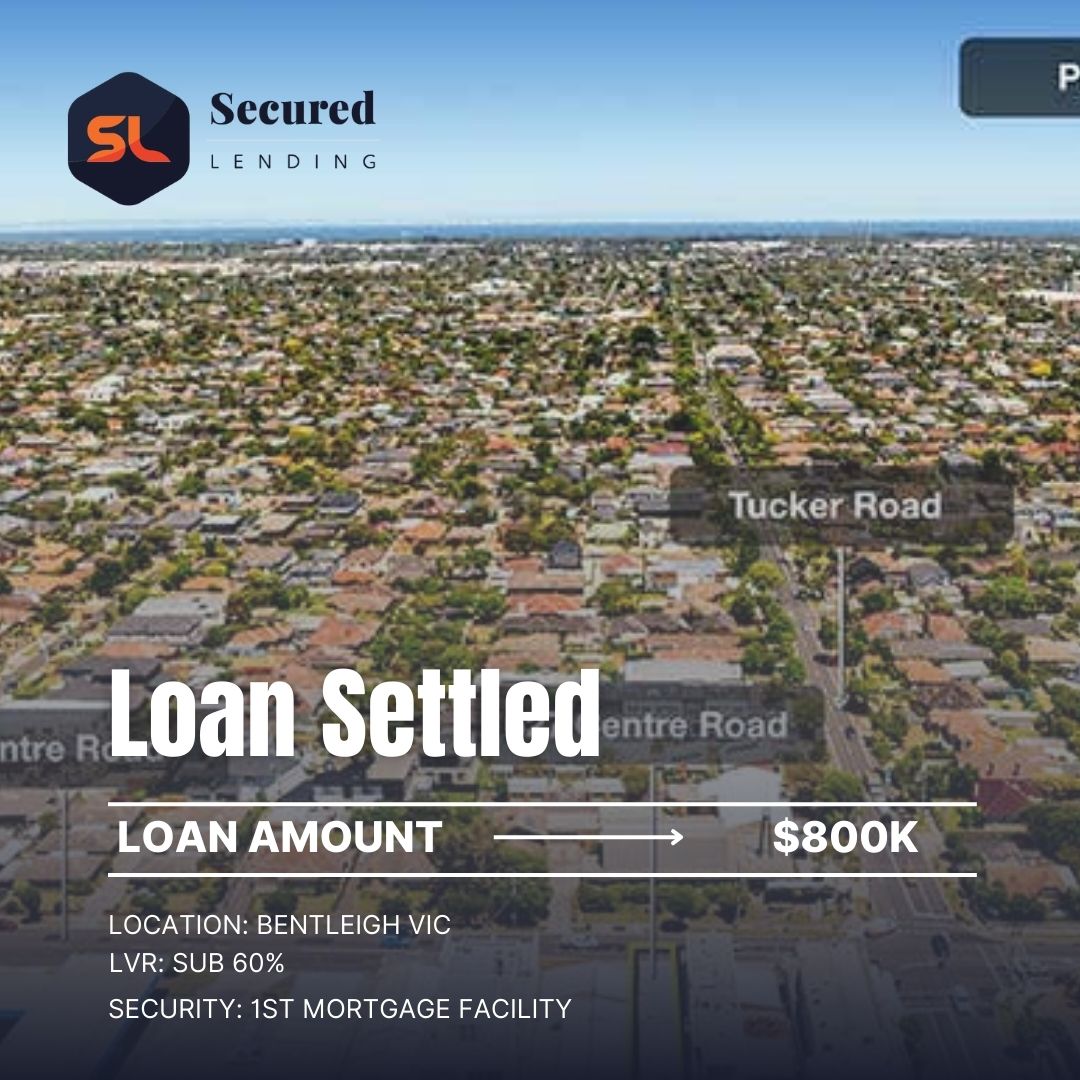

A Pty Ltd company holding a residential investment property in Melbourne needed to refinance urgently after its existing short-term facility expired and the incumbent lender stalled. Loan amount $820,000, LVR 58%. We assessed, issued a term sheet, and settled within 24 hours. The company refinanced to a lower-cost lender four months later once trading financials were in order.

A company with two existing residential investment properties needed to release $480,000 in equity from one property to fund a time-sensitive business acquisition. No full income verification was required for this structure — assessed on LVR and combined director guarantee. Funded within 72 hours of enquiry.

What to Have Ready

- •Company ABN and ACN

- •Full names of all directors and their ownership percentages

- •Address of the security property and your estimate of current value

- •Loan amount required and purpose

- •Proposed exit strategy and timeline

Related Finance Options

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.