Family trusts are the most common structure for holding residential investment property among sophisticated Australian investors. The flexibility of a discretionary trust, the ability to distribute income across beneficiaries, and the asset protection that comes with trust ownership make it a natural choice. The difficulty is that banks treat trust borrowers as more complex, often requiring the trust deed to meet specific conditions, the trustee company to have trading history, and the distribution income to be documented in a way that satisfies their serviceability model.

We lend to both discretionary and unit family trusts. The loan is made to the trustee company, with the trust property as security and personal guarantees from the directors of the trustee company. Loans range from $250,000 to $10,000,000 with same-day assessment and settlement from 24 hours for clean deals.

Where Banks Create Problems for Trust Borrowers

The main issue is how income is assessed. A discretionary trust distributes income at the trustee's discretion, which means the amount flowing to any individual beneficiary varies year to year. Banks typically apply haircuts to trust distribution income or exclude it entirely from serviceability calculations. If the primary beneficiary is also the director of the trustee company, their personal income position can look materially weaker on paper than their actual financial position.

Beyond income, trust deeds can create complications. Banks often require the trust deed to contain specific borrowing powers and trustee indemnification clauses. Older trust deeds or standard templates drafted without property borrowing in mind sometimes fail these checks, causing delays while solicitors prepare deed amendments or supplemental deeds.

Private lending sidesteps the income model entirely. We assess the security property, the LVR, the trustee's authority to borrow under the trust deed, and the exit plan. The trust deed review is practical rather than procedural — we are checking that the trustee can legally enter into the transaction, not scoring it against a compliance checklist.

Who This Is For

- •Discretionary family trusts purchasing residential investment property as a business-purpose transaction

- •Unit trusts holding or refinancing residential investment property

- •Trusts where distribution income does not satisfy a bank serviceability test

- •Trustees needing to act quickly on an auction purchase or settlement deadline

- •Trusts refinancing an existing facility to access equity or restructure terms

- •Not for owner-occupier purchases, personal use, or any borrowing in personal name

Trust Deed and Trustee Requirements

The trustee company must be properly registered and in good standing. The trust deed must confer authority on the trustee to borrow and grant security over trust assets. If the deed is silent on this or contains restrictions, your solicitor may need to prepare a supplemental deed or confirm the trustee's position at law. We flag this early in the process so it does not become a settlement issue.

All directors of the trustee company provide personal guarantees. Beneficiaries are not required to guarantee unless they are also directors. Unitholders in a unit trust may be required to guarantee depending on the deal structure — this is assessed case by case.

Three Trust Lending Scenarios

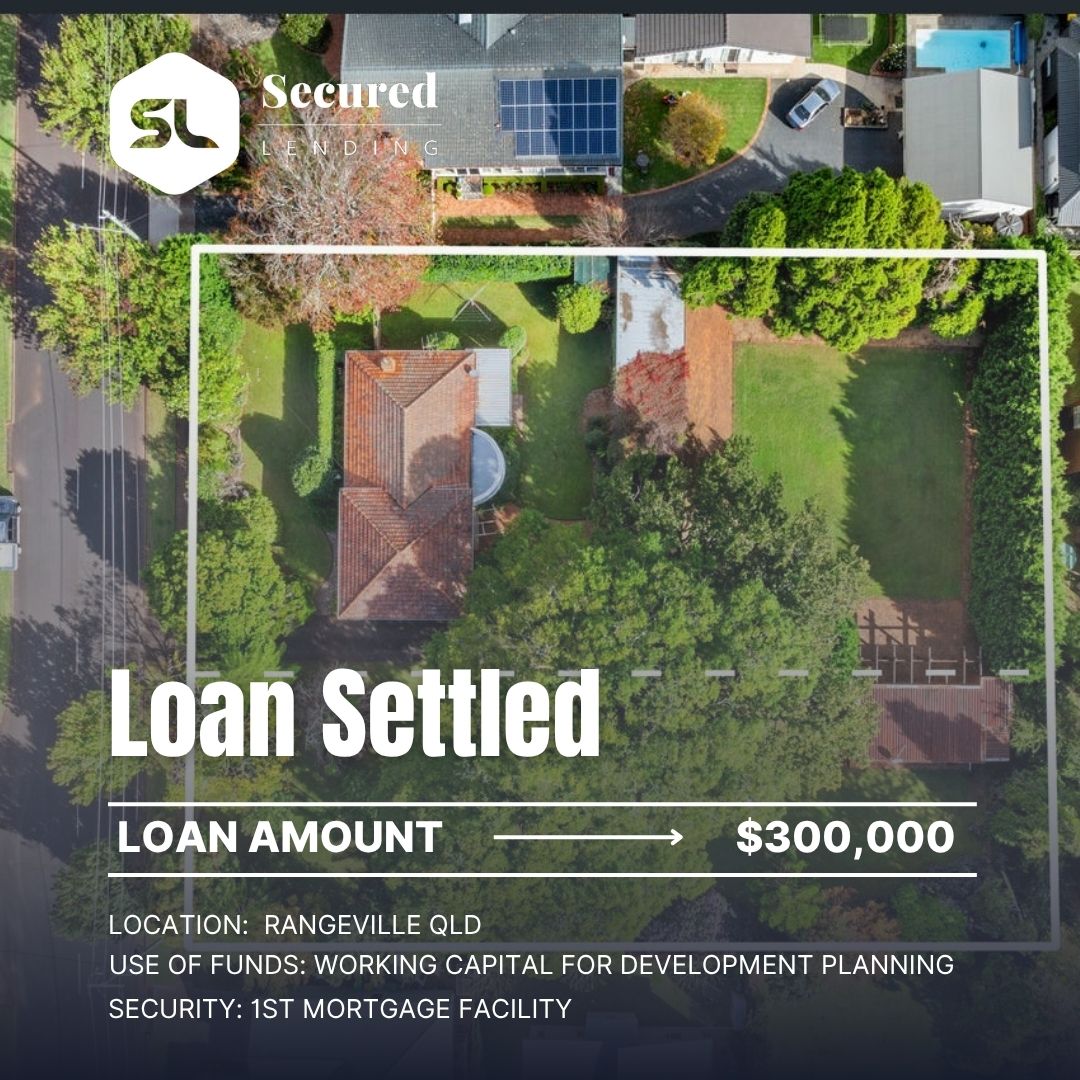

A discretionary family trust in Queensland had an accepted offer on a $1.1M residential investment property. The primary beneficiary's bank declined the trust application because her distribution income over the prior two years was inconsistent — higher in one year due to a business exit and lower the next. We assessed on the property, the LVR of 62%, and a 12-month term. Settled in 36 hours.

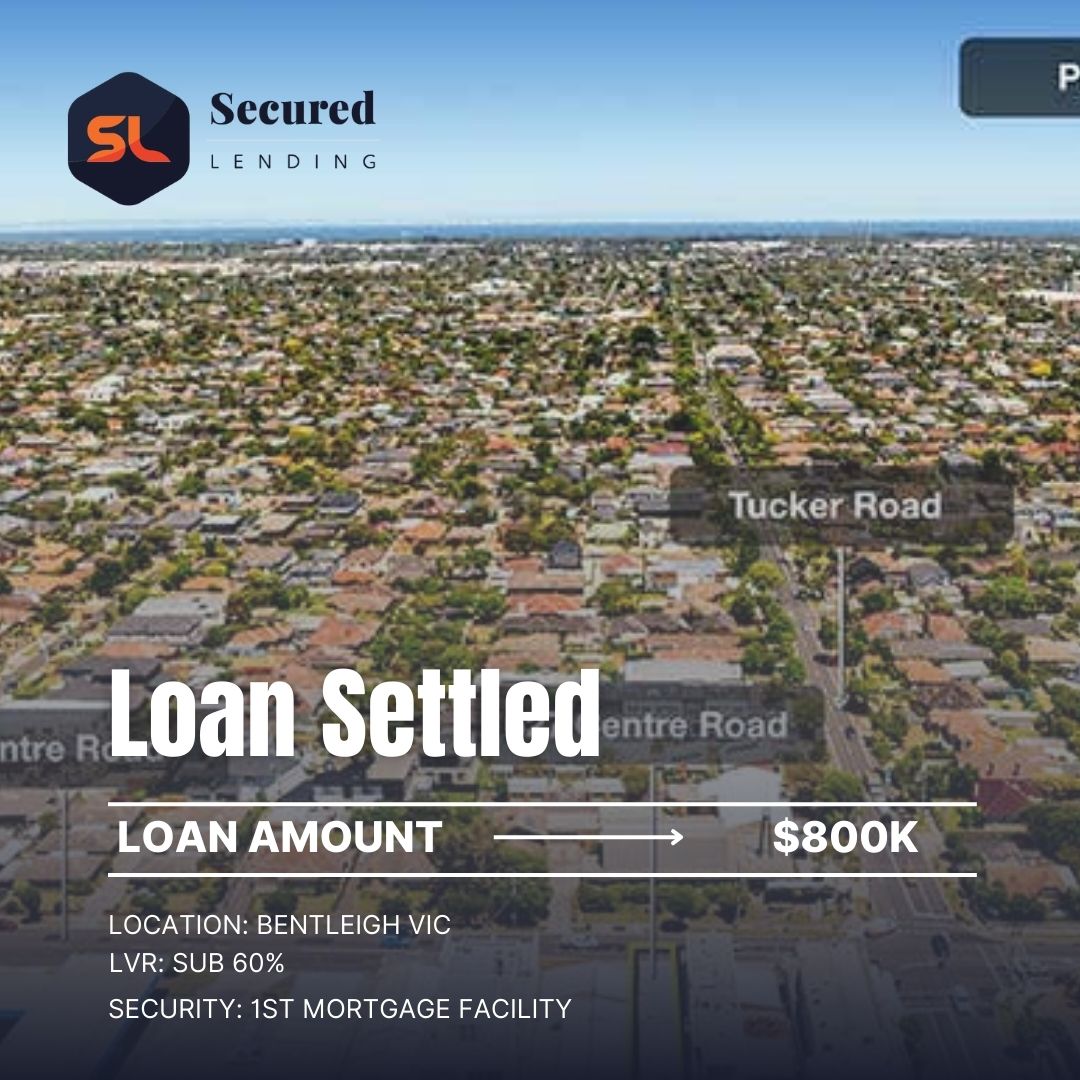

A family trust in Sydney needed to refinance a $750,000 first mortgage on a residential investment property after the original short-term lender's term expired. The trustee company had only been incorporated 18 months prior, which prevented bank refinancing. We refinanced the facility within 48 hours, giving the trustee time to establish a longer trading record before approaching a standard lender.

A unit trust with three unitholders needed $620,000 in equity released from an existing investment property to fund a commercial property deposit for one of the associated businesses. The trust had no income of its own — income flows through to unitholders. Assessed on LVR and combined unitholder guarantee. Funded within 72 hours.

Related Investment Property Finance

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.