Bridging finance for investment property is about timing. The transaction is straightforward but the sequence is wrong: you need to settle on a new investment property before your existing property has sold, before your refinance has come through, or before your bank has finished processing an application that should have been approved three weeks ago. A bridging loan fills that gap so the deal does not fall over on a timing technicality.

This page is specifically about investor bridging through corporate structures — Pty Ltd companies, family trusts, and SMSFs. It is distinct from general commercial or business bridging. The security is residential investment property, the borrower is a corporate entity, and the purpose is investment, not owner-occupied residential purchase.

When Investment Property Bridging Finance Makes Sense

- •Buying a new investment property before the sale of an existing one settles — the sale proceeds are the exit

- •Auction purchases where the 28 to 42-day settlement window is too tight for a bank approval

- •Off-market deals where the vendor requires unconditional exchange and cannot wait for finance approval

- •An existing refinance stalled in bank credit assessment, creating a settlement gap on the incoming property

- •Settlement shortfall — the long-term lender is approved but will not fund in time for the contracted settlement date

- •Chain break — another party in a related transaction is delayed, and a bridge is needed to hold your position

How the Structure Works

A bridging loan is secured by a mortgage over a residential investment property — either the property being purchased, an existing property with available equity, or both. The loan term is short, typically 3 to 12 months, and the exit is predetermined: the sale of the outgoing property, refinance to a bank or non-bank lender, or equity release from another asset in the portfolio.

Where both properties are involved — the existing one being sold and the new one being purchased — we can take security over either or both, depending on what is needed to support the loan amount and LVR. The key question we assess is whether the exit is real and achievable within the loan term.

Who This Is For

- •Pty Ltd companies purchasing residential investment property with a settlement timing gap

- •Family trusts needing to bridge between selling one investment asset and settling on the next

- •SMSFs with an LRBA purchase where settlement is compressed and the bank timeline does not fit

- •Portfolio investors managing multiple simultaneous transactions with overlapping settlement dates

- •Not for owner-occupier bridging, personal property purchases, or individuals borrowing in their personal name

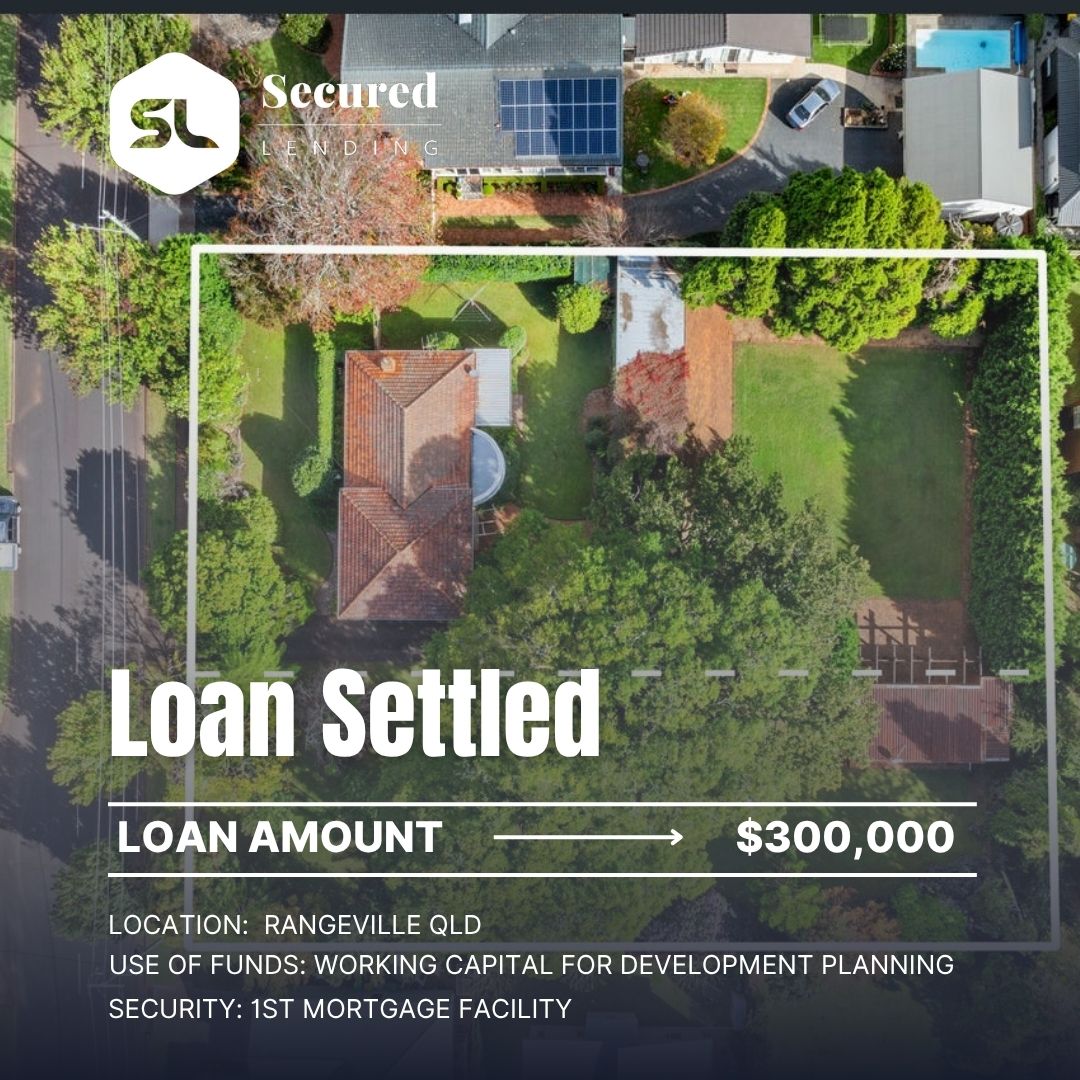

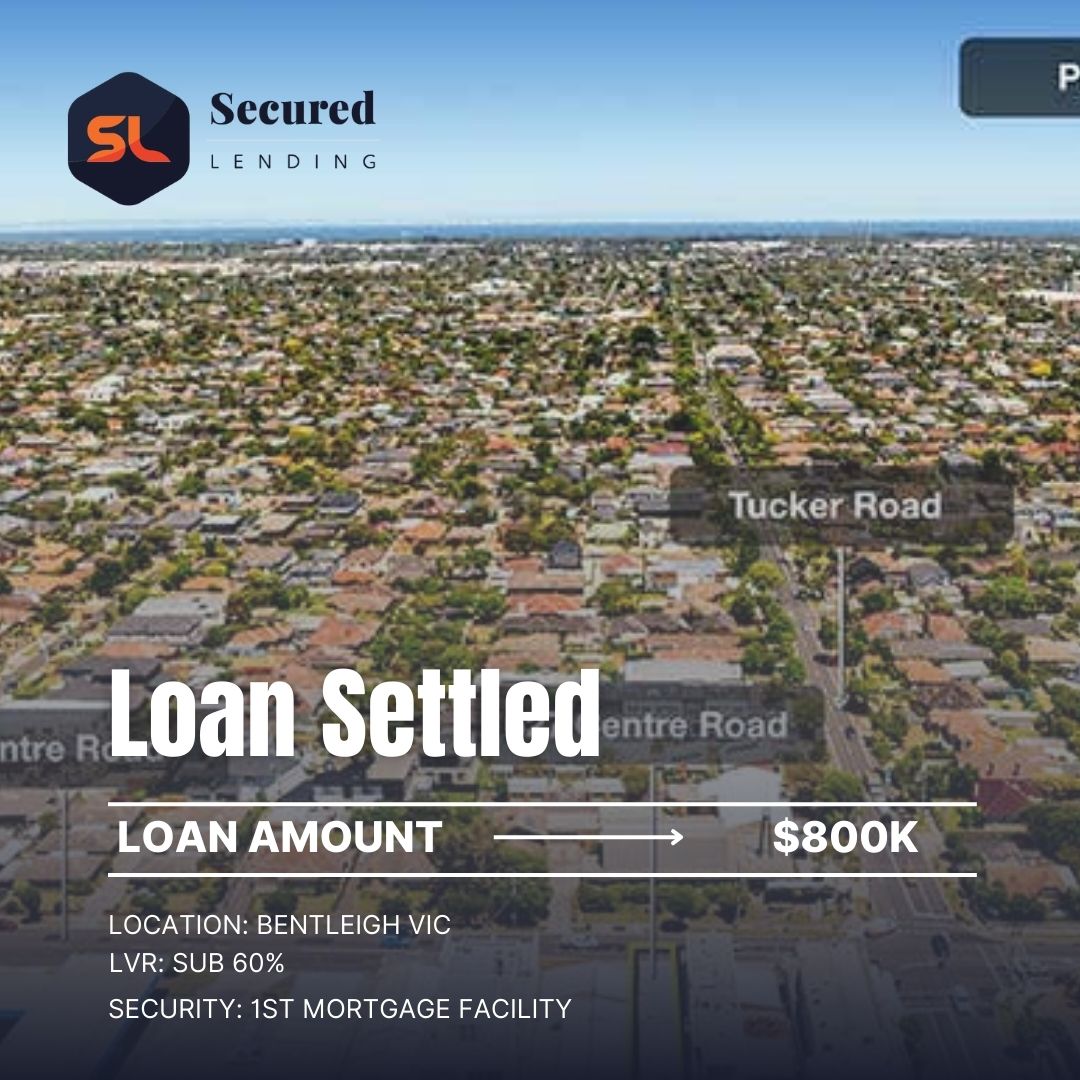

Three Investor Bridging Deals We Have Funded

A family trust in New South Wales purchased a residential investment property at auction for $1.45M. Settlement was required in 35 days. The trust's existing bank application had been in credit assessment for four weeks with no decision. We provided an indicative approval within six hours of the enquiry, issued a term sheet the following morning, and settled on day 31. The trust refinanced to its bank at the lower rate once the bank's approval came through two months later.

A Pty Ltd company needed to settle on a $920,000 residential investment property purchase before its existing investment property sold. The outgoing property was under contract but settlement was 45 days away. We bridged the gap with a 60-day facility secured against the incoming property, with the exit being the settlement proceeds from the outgoing sale. Funded within 48 hours of the contract being signed.

An SMSF had exchanged on a $780,000 residential property under LRBA. The specialist bank lender processing the SMSF application required 10 weeks minimum. Settlement was contracted at six weeks. We provided a 90-day bridging facility to fund the gap, and the fund refinanced to its long-term SMSF lender once their approval cleared.

Related Finance Options

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.