Refinancing an investment property loan to a private lender is rarely the end destination. It is almost always a strategic move to resolve an immediate problem — a facility in arrears, a lender that has issued a default notice, a short-term loan that has matured without a renewal offer, or a situation where the borrower needs time to clean up their financial position before approaching a standard lender. Private lending buys that time.

Secured Lending refinances residential investment property loans held in Pty Ltd companies, family trusts, and SMSFs. We pay out the existing lender, take a new first mortgage position, and give the borrower a structured term of 1 to 24 months to resolve whatever the underlying issue is. Loans from $250,000 to $10,000,000.

Why Investors Refinance to a Private Lender

- •The existing facility has entered arrears and the current lender is moving toward enforcement

- •A short-term or non-bank facility has matured and the lender will not renew — the borrower needs time to arrange bank finance

- •The current lender has changed its policy and no longer serves the borrower's entity structure or property type

- •The borrower wants to switch lenders but cannot satisfy a bank's income or documentation requirements yet

- •A fixed rate period has ended, the revert rate is unworkable, and break costs make immediate exit to a bank expensive

- •The borrower needs to release additional equity as part of the refinance — paying out the old lender and drawing extra funds

Refinance vs Equity Release vs Second Mortgage

These three products are often confused. Refinancing replaces the existing first mortgage entirely — the new lender pays out the old one and takes first position. Equity release can be structured as a refinance (where the new first mortgage is larger than the payout amount, returning cash to the borrower) or as a second mortgage (where the first mortgage stays in place and a new second charge is added). If you want to keep your existing first mortgage rate and just access additional funds, a second mortgage is the cleaner path. If you want to change lenders and access funds at the same time, a refinance with cashout is the right structure.

Refinancing Out of Arrears

This is where private lending refinance adds the most value. A residential investment property loan in arrears with a bank or non-bank lender creates pressure that compounds quickly — default notices, enforcement action, and ultimately mortgagee sale if the position is not resolved. A private lender refinance pays out the arrears and the outstanding balance in one transaction, removing the enforcement threat and giving the borrower a clean position to work from.

We assess arrears refinances on the property value, the payout amount, the resulting LVR, and the borrower's plan to exit private lending at term end. The fact that the borrower is in arrears is not itself a reason to decline — we understand that arrears positions often arise from circumstances rather than from a fundamental problem with the asset or the borrower.

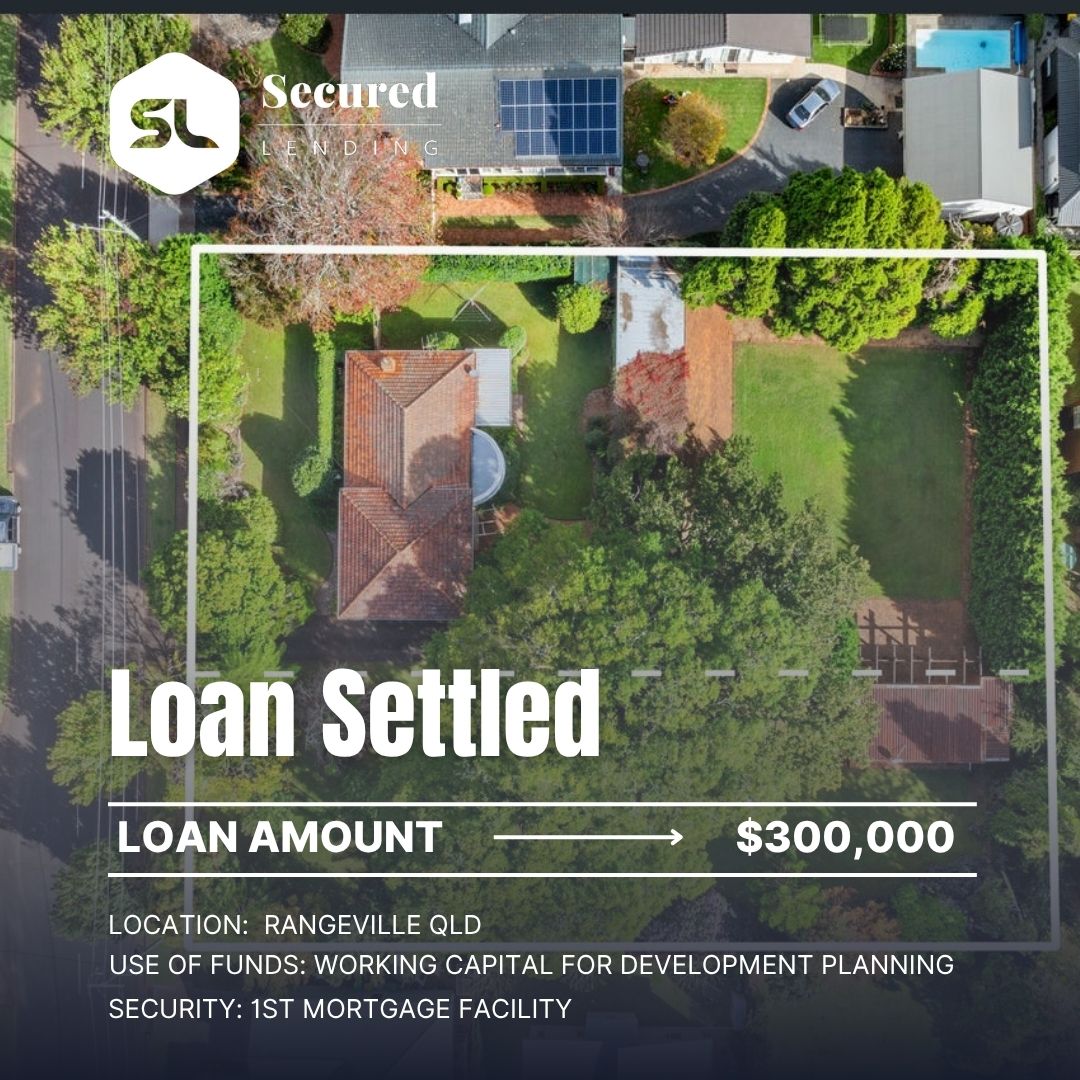

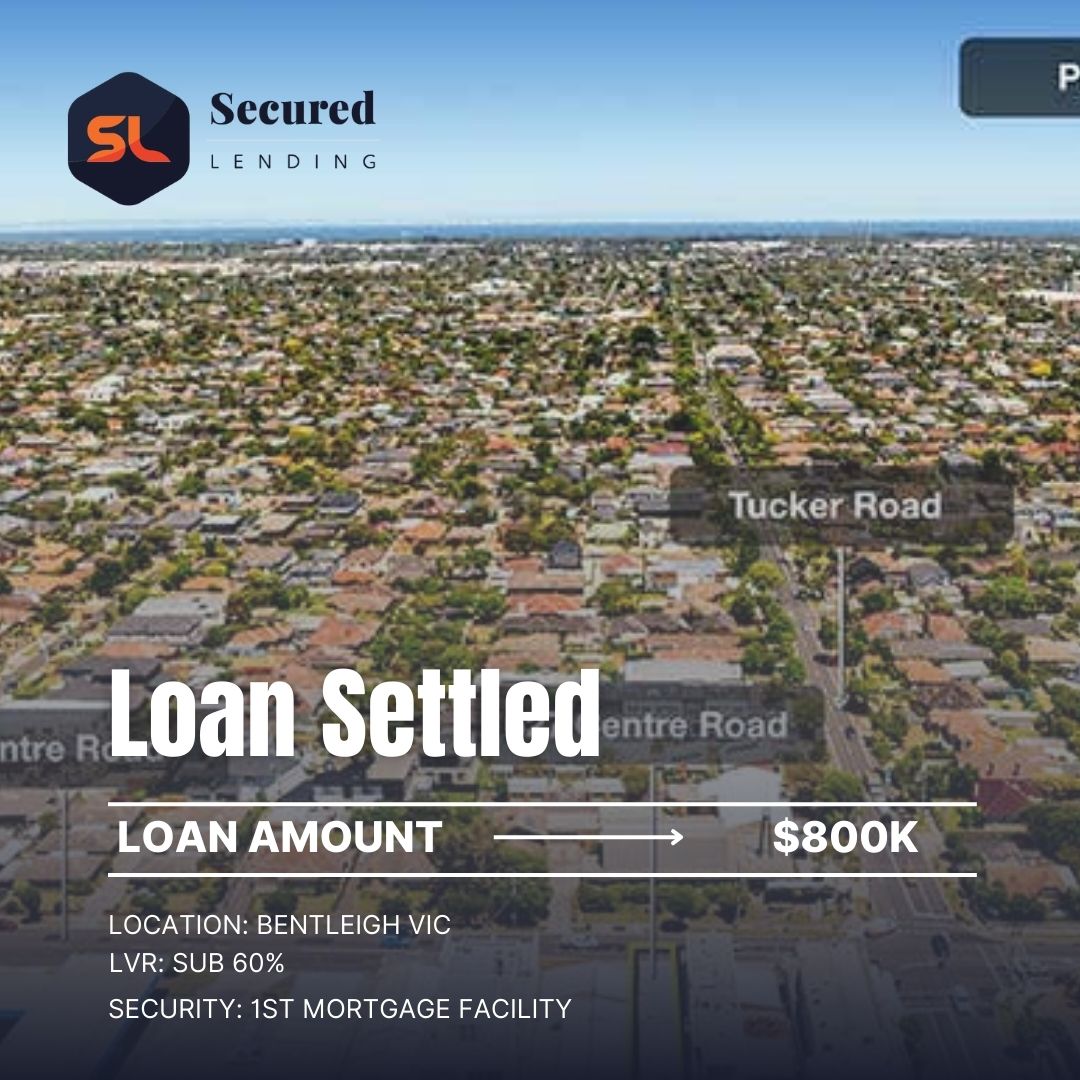

Three Refinance Deals We Have Funded

A Pty Ltd company had a residential investment property in Sydney worth $1.7M with an existing $980,000 mortgage that had entered arrears following a period of vacancy. The bank had issued a formal default notice. We paid out the bank in full, including accrued default interest and legal costs, and provided a 12-month facility at 62% LVR. The company resolved the arrears position, found a new tenant, and refinanced to a non-bank lender at month nine.

A family trust had a 12-month facility from a private lender that matured. The original lender declined to renew, citing a policy change around trust borrowers. Loan balance $640,000 against a Brisbane residential investment property worth $1.05M. We refinanced the position within 36 hours of the enquiry, giving the trust eight months to arrange bank finance with the urgency removed.

An SMSF had a maturing LRBA facility and its incumbent specialist lender had raised its rates materially at renewal. The fund wanted to exit and refinance to a more competitive long-term SMSF lender, but that lender's approval timeline was 10 weeks. We bridged the position for 90 days, the fund's new lender settled on schedule, and the SMSF moved to its long-term facility without a gap.

Related Finance Options

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.