Equity that sits in a residential investment property is productive only when it is working. A portfolio investor who bought well five years ago may have $1.5M in equity across two properties, but if that equity is locked in and inaccessible, it cannot fund the next acquisition, cover a business opportunity, or be deployed for any other purpose. Equity release is the mechanism for making that capital available without selling the asset.

We lend against existing residential investment property held by Pty Ltd companies, family trusts, and SMSFs, releasing equity as a cash facility. The property stays in the portfolio. The borrower accesses funds for investment or business purposes. The loan is repaid or refinanced at term end. All borrowing must be for genuine business or investment purposes — not for personal, domestic, or household use.

When Investors Use Equity Release

- •Funding the deposit or full purchase price of a next investment property in the portfolio

- •Injecting working capital into a related business during a growth phase or cash flow gap

- •Bridging a gap while a longer-term refinance or asset sale is arranged

- •Accessing funds before the end of financial year for tax or structuring purposes

- •Releasing equity from one trust-held property to fund activity in a related entity

- •Paying out a co-investor or restructuring ownership within a portfolio

How the Loan Is Structured

Equity release is delivered as a first or second mortgage over the existing residential investment property. If the property is unencumbered, we take a first mortgage and release the agreed loan amount. If there is an existing first mortgage in place, we take a second position and release equity on the basis of the combined LVR. Our standard maximum LVR is 70% — meaning if the property is worth $1.4M and the existing first mortgage is $500,000, there may be up to $480,000 available depending on deal specifics.

Loan terms run from 1 to 24 months. Most equity release deals are structured as 6 to 12-month facilities, with the borrower refinancing to a standard lender once the purpose has been achieved and the financial position allows it.

The Difference Between Equity Release and Refinancing

Refinancing replaces an existing facility with a new one — a new lender pays out the old one, and the borrower starts fresh with new terms. Equity release adds a new facility on top of, or instead of, an existing one, with the purpose being to extract cash from the property. If there is no existing mortgage, an equity release is a new first mortgage drawing out cash. If there is an existing mortgage that the borrower wants to leave in place, equity release takes second position. See the refinance page and the second mortgage page for those scenarios in more detail.

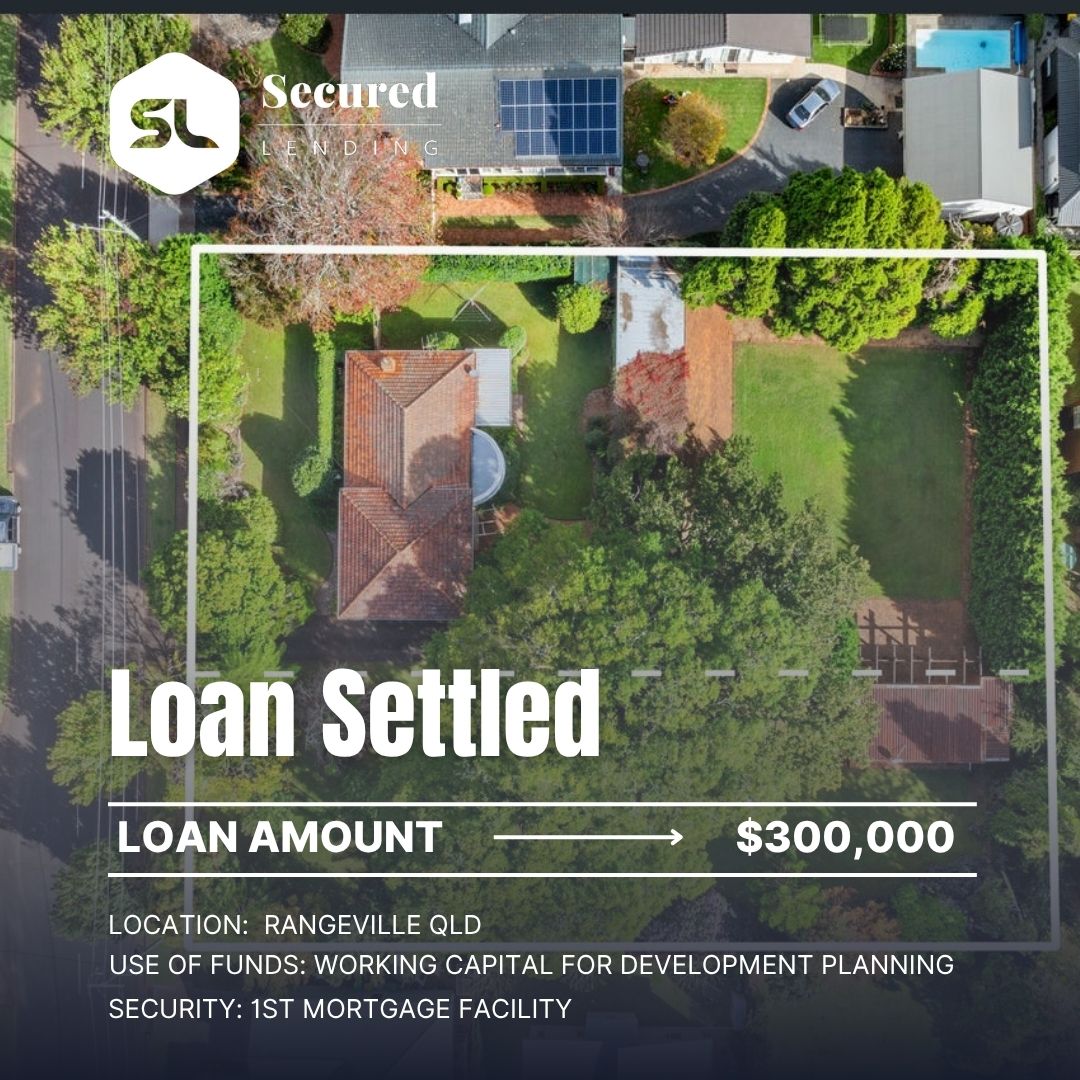

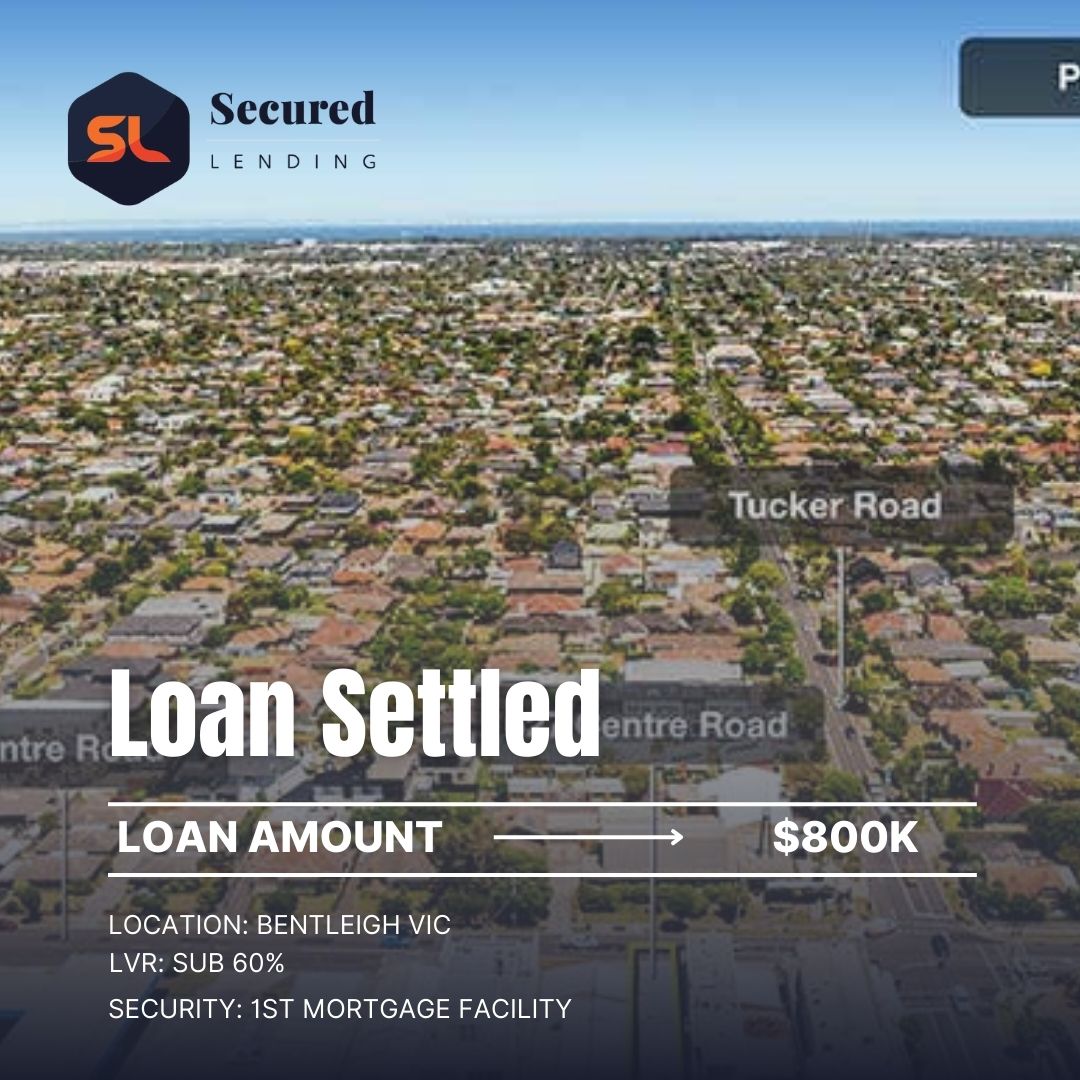

Three Equity Release Deals We Have Funded

A family trust owned a residential investment property in Melbourne worth $1.8M with no existing mortgage. The trustee needed $600,000 to fund the deposit on a commercial property purchase in another entity. We released $600,000 as a 9-month first mortgage at 44% LVR, with exit via refinance to a non-bank lender once the commercial purchase was complete and the trust's overall debt position was consolidated.

A Pty Ltd company with a residential investment property in Brisbane worth $1.1M and an existing bank first mortgage of $390,000 needed $320,000 in working capital for its construction business. We took a second mortgage position at a combined LVR of 65%, funded within 48 hours. The company repaid the second mortgage from business cash flow over 11 months.

A two-property portfolio held in a discretionary trust had combined equity of $1.9M against combined debt of $680,000. The trustee needed $450,000 to buy out a departing beneficiary. We structured a cashout refinance over the stronger of the two properties at 58% LVR, settled in 36 hours, and the trust refinanced the position to its bank six months later once the buyout documentation was in order.

Related Finance Options

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Short Term Loans

Flexible property-secured loans designed for businesses that need capital now and a clear exit path later. Ideal for bridging gaps, seizing opportunities, or managing short-term pressure.