When a commercial or investment purchase in Adelaide turns on the settlement date, the lender that funds it has to move at the pace of the contract. Secured Lending writes first and second mortgages over property to do exactly that, from $250,000 to $10 million, drawn from our own capital and able to settle a clean file inside 24 hours. We back buyers and investors across the metropolitan area and the regions, and we lend only for business and investment, never an owner-occupied home or any consumer credit.

Settling an Adelaide purchase before the bank is ready

Commercial and investment buys around the CBD and North Adelaide, industrial acquisitions out at Wingfield, Edinburgh Parks, and Lonsdale near the Osborne and Tonsley precincts, and vineyard or winery property through the Barossa and McLaren Vale all tend to come with a fixed settlement and a vendor who will not wait. A bank weighs the borrower against a serviceability model and a credit queue; we weigh the property going up as security and the plan to repay it. That swap lets us commit to a purchase a bank is still assessing, and fund it on time.

- •First and second mortgages from $250,000 to $10 million, clean purchases funded within 24 hours

- •Assessed on the asset and a credible exit, not a serviceability score or three years of returns

- •Rates from 9.7% p.a. over terms of 1 to 24 months

- •Approved in-house, so no credit committee sits between your offer and settlement

- •Strictly business and investment use, never an owner-occupied home or consumer loan

Buying commercial and investment property in Adelaide

Funding the purchase is where most of our Adelaide book sits. We settle commercial buys, an owner-occupied premises, a tenanted office, a retail strata suite, an industrial shed in the northern corridor, and we fund investment purchases for the companies, trusts, and SMSFs that investors buy through and that banks are slowest to clear. With our own valuation team and our own funds, a purchase can settle in as little as 24 to 48 hours, so the right asset does not slip while a bank works through its process.

Holding the first registered charge

A first mortgage puts us in the primary security position, which earns our sharpest pricing: rates from 9.7% p.a. and LVRs reaching 75% on a strong Adelaide asset, over terms of one to twenty-four months. Buyers reach for it to settle a purchase against a hard date, to refinance a facility that no longer fits, or to draw working capital against an unencumbered building. Because the funds are ours, nothing sits between an agreed offer and the day the money lands.

Drawing on equity through a second mortgage

Where a bank loan already sits on the property, a second mortgage ranks behind it and releases the equity without refinancing or paying that loan out, with combined borrowing generally held to 75% of value. It is the tool when the equity is clearly there and the timing is tight: a deposit on the next acquisition, a short bridge between settlements, or a working-capital gap that needs covering while the first facility stays in place. We will take a second position behind both bank and non-bank lenders.

The part of a purchase we weigh hardest

Four things decide whether we fund a purchase, and the exit carries by far the most weight. A mortgage is only as sound as the plan to clear it, so we want that route mapped in plain terms before anything else moves.

- •The exit: a dated, evidenced path to repay, by sale, a refinance back to a bank, or a known incoming payment. Nothing weighs more

- •The security and the loan against it: current market value, with the LVR generally topping out near 70%

- •The purpose: a genuine commercial or investment reason for the purchase or the draw

- •The title and our ranking: clear title, and whether we register a first or second mortgage

Property we will take as security

The mortgage funds the business or the investment; the property is what backs it. Our own valuers price each asset against current Adelaide and regional comparables, which is quicker and closer to the real number than waiting on an outsourced desktop figure.

- •Investment housing and units across the metropolitan area, North Adelaide through the inner suburbs

- •Offices, retail, and strata suites in the CBD and the surrounding commercial belt

- •Warehousing and light industrial across Wingfield, Edinburgh Parks, Lonsdale, and the northern corridor

- •Vineyard, winery, and agribusiness property through the Barossa, McLaren Vale, the Adelaide Hills, and Clare

- •Vacant land and development sites, DA approved or not

- •Property with a bank loan still in place, taken on behind it as a second mortgage

- •Assets bought and held inside a company, trust, or SMSF

“A purchase in Adelaide lives and dies on the settlement date. The vendor will not move it, and a bank cannot always meet it, so the buyer with a clean property and a clear way out needs a mortgage that funds to the calendar. Bring us the deal early and we will tell you the same day whether we can settle it on time.”

Gino Tabila

Associate Director

Where we fund purchases across Adelaide and the regions

We register first and second mortgages right through the metropolitan area, from the CBD and North Adelaide out across the inner suburbs and the industrial corridors at Wingfield, Edinburgh Parks, and Lonsdale. Beyond the city we fund purchases in the wine country and the agricultural districts, the Barossa, McLaren Vale, the Adelaide Hills, and Clare among them. Wherever the property you are buying or borrowing against sits in the area, we can usually move on it quickly.

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

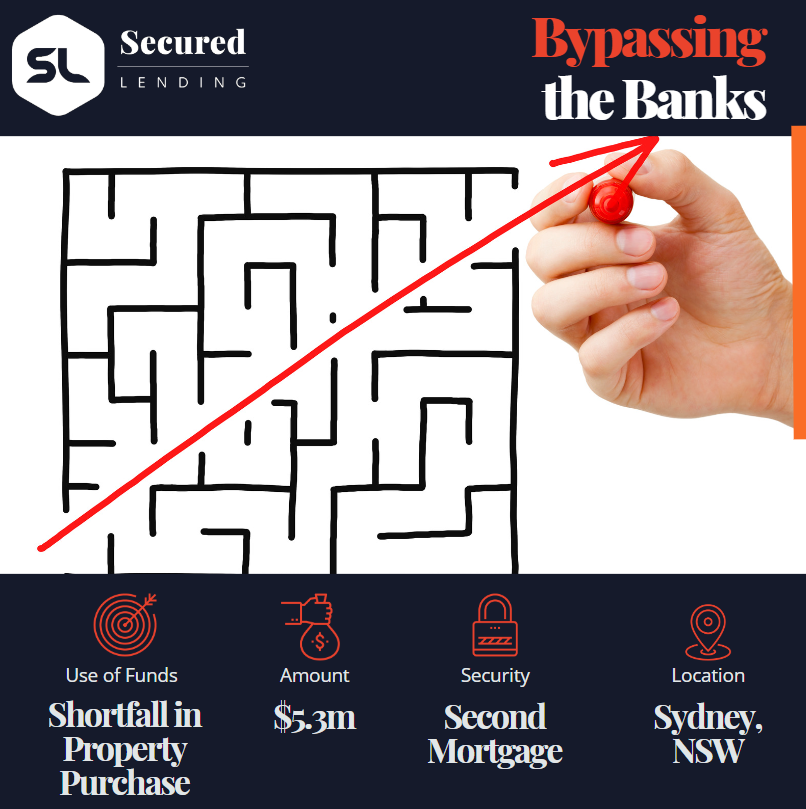

$1.9M Commercial Property Acquisition for Growing Doggy Daycare Business

$3.5M First and Second Mortgage in Cronulla: Seizing an Investment Opportunity in Days

How We Delivered a $13M First Mortgage in Just 48 Hours

$1.2M Second Mortgage Approved in 24 Hours: Unlocking Equity for a Time-Sensitive Commercial Deal

$3M Working Capital for IT Business Expansion Settled in 2 Business Days

$1.15M ATO Debt Cleared in 4 Business Days for Prahran Pub Operator

$250K Working Capital for Brisbane Café in 36 Hours

Successful $5.7M Blended Loan: When First and Second Mortgages Work Together

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Refinance

Replace an existing loan that is maturing, under pressure, or no longer working. We move fast and lend where banks won't.