Buying property on the Gold Coast often turns on who can fund the purchase fastest, and that is the gap a private mortgage fills. Secured Lending writes first and second mortgages from its own book to settle commercial, investment, and development buys across the coast, with facilities running from $250,000 to $10 million that a clean file can fund within 24 hours. We are a non-bank lender working out of Barangaroo, Sydney, and the money is strictly for business and investment use. We do not write owner-occupied home loans or any consumer credit.

Buying a going-concern hospitality or tourism freehold

A large slice of Gold Coast property changes hands tied to tourism and hospitality, the beachfront venues, restaurants, and accommodation freeholds that earn in seasonal waves around the holidays and the event calendar. A bank treats those waves as a serviceability problem and smooths a year of takings into one figure it can reject. We price the purchase on the asset and the exit instead, so a going-concern buy with a quiet off-season behind it is not penalised. Whether you are settling the freehold, the going concern, or both, we register a first or second mortgage and move on the contract date rather than a committee's.

Taking the primary charge with a first mortgage

Hold the first registered mortgage and we sit in the primary security position, which carries the lowest risk and our keenest pricing: rates from 9.7% p.a., LVR to 75% on a strong coast asset, and terms of one to twenty-four months. Coast buyers reach for a first mortgage to settle a commercial or development-site purchase against a fixed date, to refinance a facility that no longer fits the plan, or to fund a larger acquisition where the title is clear. The structure is built around when your exit lands.

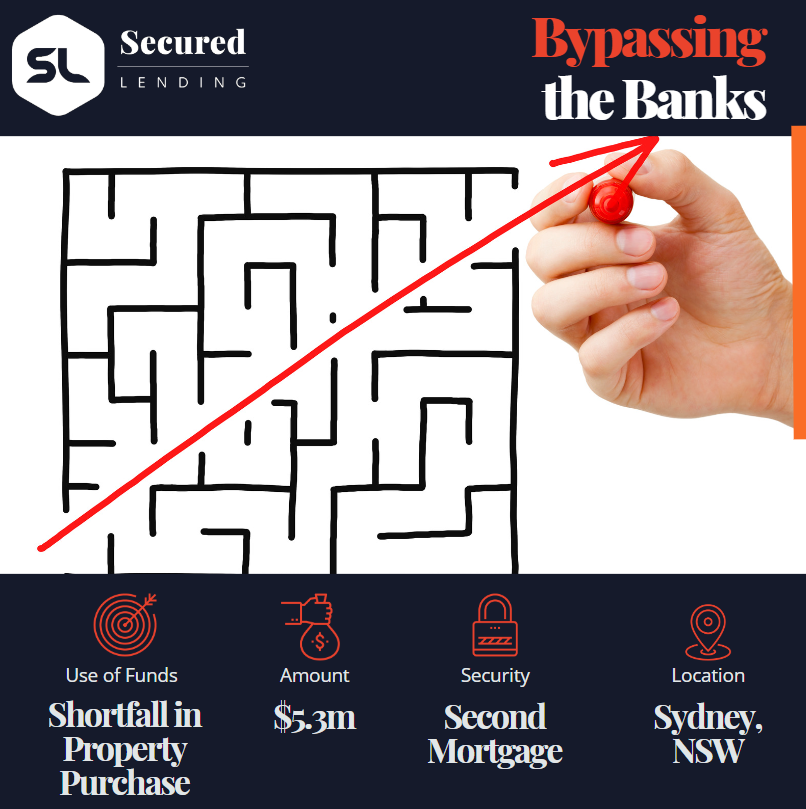

Drawing equity with a second mortgage

A second mortgage ranks behind a bank loan you already carry, letting you pull equity out of a coast property to fund the next purchase without refinancing or disturbing that first facility. Combined borrowing is generally held inside 75% of value. It is the tool when the equity is plainly sitting there and the timing is tight, covering a deposit on the next site, a settlement shortfall, or a short bridge between a development stage and its sell-down.

Funding development and construction purchases

The coast development pipeline keeps us busy, from a high-rise on the Surfers strip to the master-planned releases at Coomera and the corridor running north. We fund the land acquisition, the settlement shortfall, and short bridges between stages, secured against the site or the completed stock. Our valuers are comfortable pricing a partly built project, a land bank, or a staged subdivision, which is exactly where a bank tends to stall. Commercial buyers at Southport, Robina, and Surfers Paradise, and industrial buyers chasing M1 sheds, use the same speed to settle on time.

How we weigh a purchase

Four things decide whether a buy works, and the exit sits above the rest. A mortgage is only ever as sound as the plan to clear it, so we want that route mapped, in plain terms, before anything else.

- •The exit: a dated, evidenced way to repay, by sale, sell-down, refinance to a bank, or known incoming funds. Nothing outweighs it

- •The security and the loan against it: current market value and an LVR that generally tops out near 70%, with more on the strongest assets

- •The purpose: a genuine business or investment buy, never a personal or consumer one

- •Title and ranking: clean title, and whether we take the first or the second mortgage

Coast property we will secure a purchase against

The mortgage funds the purchase; the property is what backs it. Our own valuers price each asset against current coast evidence, faster and sharper than waiting on an outsourced desktop figure, and we are at ease with assets held through investment structures.

- •Going-concern hospitality and tourism freeholds, including accommodation and venue buys

- •Commercial offices, retail, and strata suites at Southport, Robina, and Surfers Paradise

- •Investment apartments and held residential in Surfers Paradise, Broadbeach, and Robina

- •Industrial sheds and warehouses along the M1 estates that run the length of the city

- •Development sites and vacant land across Coomera and the master-planned northern releases, with or without a DA

- •Purchases settled inside a Pty Ltd company, a trust, or an SMSF

“On the coast the deal is usually won on settlement day, not on rate. A buyer who can fund a freehold or a development site the moment it goes unconditional beats the one still waiting on a bank to model a season of takings. Hand us a sound property and a clear way out, and that buyer is you.”

Gino Tabila

Associate Director

Where we settle purchases across the coast

We fund first and second mortgages the length of the Gold Coast, from the Surfers Paradise and Broadbeach high-rises through the commercial cores at Southport and Robina, out to the master-planned growth at Coomera and the corridor north, and across the M1 industrial estates in between. Buy a hospitality freehold on the water, settle a development site inland, or release equity to fund the next acquisition, and we can move on it quickly. If the property you are buying sits in Queensland, we want to hear from you.

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

$1.9M Commercial Property Acquisition for Growing Doggy Daycare Business

$3.5M First and Second Mortgage in Cronulla: Seizing an Investment Opportunity in Days

How We Delivered a $13M First Mortgage in Just 48 Hours

$1.2M Second Mortgage Approved in 24 Hours: Unlocking Equity for a Time-Sensitive Commercial Deal

$3M Working Capital for IT Business Expansion Settled in 2 Business Days

$1.15M ATO Debt Cleared in 4 Business Days for Prahran Pub Operator

$250K Working Capital for Brisbane Café in 36 Hours

Successful $5.7M Blended Loan: When First and Second Mortgages Work Together

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Refinance

Replace an existing loan that is maturing, under pressure, or no longer working. We move fast and lend where banks won't.