Secured Lending writes first and second mortgages on Eastern Suburbs property for investors, operators, and companies moving on a purchase or an equity release that a bank cannot match for pace. We lend our own capital, from $250,000 to $10 million, strictly for business and investment purposes, never owner-occupied home loans or consumer credit. The high values across Bondi, Double Bay, Vaucluse, Bellevue Hill, and Rose Bay make strong first and second mortgage security, and a clean file can settle within 24 hours. We run the desk from Barangaroo, minutes across the city from the east.

Buying commercial and investment property in the east

A large share of our Eastern Suburbs lending funds purchases: a hospitality or boutique retail freehold in Bondi Junction, a strata commercial suite in Double Bay, or an investment apartment in Bondi bought to hold. Where a bank routes the deal through a credit committee and an outsourced valuation, we issue a letter of offer quickly and instruct our own valuers, so your offer carries a speed a bank cannot match. Most investors here buy through a trust, a Pty Ltd company, or an SMSF, and those are exactly the structures we are set up to fund without the delay a bank adds.

Taking a first mortgage on an Eastern Suburbs asset

Holding the first registered mortgage puts us in the lead security position, and that is where the pricing is sharpest: rates from 9.7% p.a. and LVR up to 75% on a strong asset. Borrowers here reach for a first mortgage to settle a purchase against a hard date, to refinance a facility that no longer suits, or to free working capital from an unencumbered residential or commercial holding in Vaucluse, Rose Bay, or Bellevue Hill. Terms run one to twenty-four months, shaped around when your exit lands.

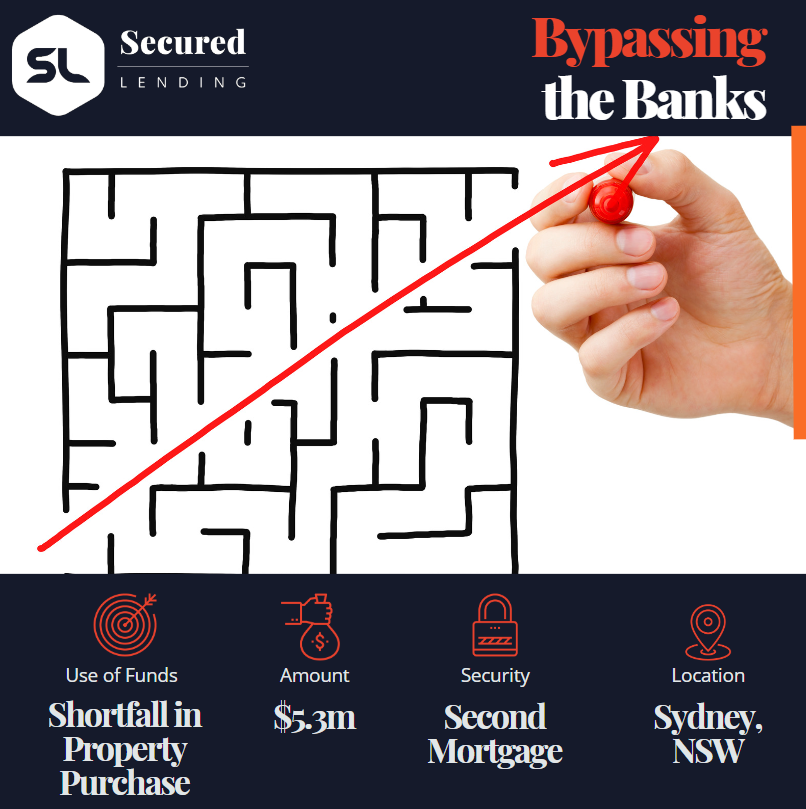

Releasing equity behind a bank with a second mortgage

A second mortgage ranks behind the bank facility you already hold, so you can pull equity out of a premium Double Bay or Rose Bay property without refinancing or paying out that first loan. Combined borrowing is generally kept within 75% of value. For high-net-worth owners it is the tool of choice when the equity is plainly there and the timing is tight, whether the funds cover a deposit on the next purchase, a short bridge, or working capital for the business.

Why the bank serviceability test fails sophisticated borrowers

High-net-worth investors and operators in the east rarely fit a serviceability calculator. Income earned through trusts and companies, billed in lumps, or paid as a self-employed professional gets flattened into one annual figure a bank wants to see, even when the borrower holds millions in equity in a Bellevue Hill or Vaucluse asset. A purchase against a deadline or an equity release for the business will not wait for that process. We decide on the property offered as security and a credible plan to repay, which is why a borrower a bank cannot model is often straightforward for us.

- •First and second mortgages from $250,000 to $10 million, clean files funded inside 24 hours

- •Assessed on the security and a believable exit, not a serviceability model or years of financials

- •Built for the trust, company, and SMSF structures Eastern Suburbs investors actually buy through

- •Approved in-house, so no credit committee stands between your offer and settlement

- •Rates starting at 9.7% p.a., on terms running from 1 to 24 months

- •For business and investment purposes only, never an owner-occupied home loan

Security we lend against across the east

The funds back your purchase or your business; the property stands behind them. Our own valuers price each asset against current Eastern Suburbs sales, which is faster and sharper than waiting on an outsourced desktop figure.

- •Premium residential: an investment property, apartment, or held dwelling in Vaucluse, Rose Bay, Bellevue Hill, Double Bay, or Bondi

- •Hospitality and boutique retail freeholds around Bondi, Bondi Junction, and the eastern beaches

- •Strata commercial and office suites through Double Bay and Bondi Junction

- •Vacant land and development sites, DA approved or not

- •Property held inside a trust, company, or self-managed super fund

- •Property that still carries a bank facility, taken behind it as a second mortgage

The factors that decide your mortgage

We weigh five things on every file, and the exit outranks the rest by a wide margin. A mortgage is only as sound as the way you clear it, so we want that route mapped first, in plain terms, ahead of anything else.

- •The exit: a dated, evidenced way the loan is repaid, through a sale, a refinance to a bank, or funds coming in. Nothing else comes close

- •The security and the loan against it: current value and an LVR usually capped near 70%, up to 75% on strong first mortgage security

- •The purpose: a genuine business or investment reason, such as a purchase, a refinance, or an equity release

- •The title and our ranking: clean title, and whether we take a first or second mortgage

- •The wider picture: the surrounding circumstances that make your exit credible

“Buyers in the east are often competing on a premium freehold or apartment where the winning offer is the one that can settle, not the one that waits weeks on a bank. With a strong property and a clear way out, we can hold a first or second mortgage position and have you funded while a committee is still reading the file.”

Gino Tabila

Associate Director

Where we fund mortgages across the Eastern Suburbs

We write first and second mortgages right across the east, from the premium residential pockets of Vaucluse, Bellevue Hill, Rose Bay, and Double Bay to the hospitality and retail freeholds of Bondi and Bondi Junction, and out through Woollahra, Paddington, Randwick, Coogee, Maroubra, and the eastern beaches. Whether you are buying a commercial or investment property or releasing equity behind an existing loan, if the property sits in the Eastern Suburbs we can usually act fast.

Frequently Asked Questions

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Case Studies

$1.9M Commercial Property Acquisition for Growing Doggy Daycare Business

$3.5M First and Second Mortgage in Cronulla: Seizing an Investment Opportunity in Days

How We Delivered a $13M First Mortgage in Just 48 Hours

$1.2M Second Mortgage Approved in 24 Hours: Unlocking Equity for a Time-Sensitive Commercial Deal

$3M Working Capital for IT Business Expansion Settled in 2 Business Days

$1.15M ATO Debt Cleared in 4 Business Days for Prahran Pub Operator

$250K Working Capital for Brisbane Café in 36 Hours

Successful $5.7M Blended Loan: When First and Second Mortgages Work Together

Get an indicative offer within hours, not weeks.

No credit check. No obligation.

Why Secured Lending?

Scenarios We Can Help With

Browse our full range of services, industries, locations, and resources to find the right financial solution for your needs.

Our Loan Solutions

Bridging Finance

Short-term funding to bridge the gap between a property purchase and a longer-term finance solution.

First Mortgage

Private first mortgage loans secured against residential, commercial, or industrial property.

Second Mortgage

Unlock equity in your property without refinancing or disturbing your existing first mortgage.

Caveat Loans

Urgent caveat loans secured by property. No need to refinance your existing mortgage.

ATO Tax Debt

Fast funding to help businesses resolve ATO obligations before penalties, garnishees, or director penalty notices escalate.

Debt Consolidation

Roll multiple high-rate facilities into one property-backed loan. Simplify repayments and restore cash flow.

Urgent Business Loans

When timing is critical and banks can't move fast enough, we step in. Property-secured funding for businesses that need an answer today — not next week.

Refinance

Replace an existing loan that is maturing, under pressure, or no longer working. We move fast and lend where banks won't.